Business

Fed set to hike rate again as consumer confidence in economy hits 2-year high

Media Landscape

This story is a Media Miss by the left as only 30% of the coverage is from left leaning media.

Learn more about this dataLeft 30%

Center 30%

Right 40%

Bias Distribution Powered by Ground News™

Whatever happened to that recession? Several months ago, top economists predicted the country would be in a recession right now. Instead, consumer confidence just hit a 2-year high in July, the U.S. unemployment rate is 3.6%, and gross domestic product numbers due this week are expected to show a growing economy for the second quarter of 2023.

A large majority of surveyed business economists – 71% – now say the odds of the U.S. entering a recession in the next 12 months are 50% or less, according to the latest National Association of Business Economics survey.

Fitch Ratings was among the leading agencies predicting a recession by the second quarter of 2023. Now, updated forecasts point to a mild recession in the last quarter of the year and the first quarter of 2024.

“The bottom line is that this is a very resilient economy and the strength of the labor market has surprised everybody,” said Olu Sonola, head of U.S. Regional Economics at Fitch Ratings. “There’s a possibility that may actually continue, even though we think the labor markets would weaken from the third quarter going out through to 2024.”

Fed set to hike rate again

After pausing rate hikes in June, the overall consensus is that the Federal Reserve will again hike the federal funds target rate on Wednesday, July 26. It currently sits between 5% and 5.25%, whereas a hike will bring the borrowing rate to 5.25% to 5.5%.

“It seems like it may be one and done because inflation numbers have been surprisingly lower than expected. We’re at 3% now. Nobody actually thought we’d be at 3% this quickly,” Sonola told Straight Arrow News. “But I think the Fed will be paying a lot more attention to core inflation, which is still more than double its target.”

For that reason, Sonola said they cannot rule out another rate hike later in the year. Fitch Ratings currently predicts the Fed will start cutting rates around March 2024, with inflation at around 2.5% to 3%.

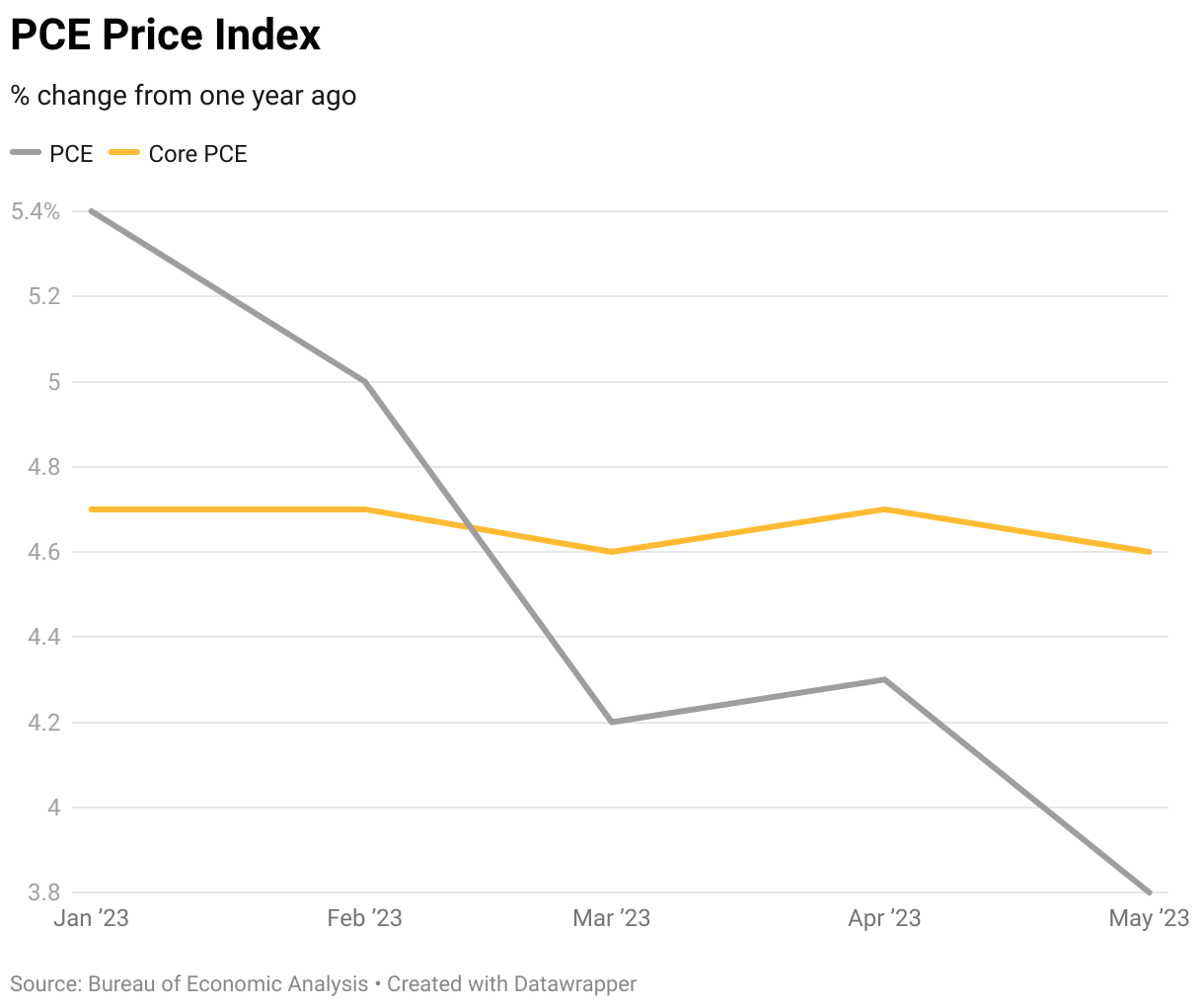

Lower headline inflation distorting true inflation picture

Despite significant declines in headline inflation numbers from the consumer price index and personal consumption expenditures price index, core inflation is proving much sticker.

In the Fed’s preferred inflation gauge, PCE, core prices, which exclude more volatile food and energy indexes, have barely budged all of 2023. While overall annual PCE has gone from 5.4% in January to 3.8% in May, core PCE has hardly moved, from 4.7% in January to 4.6% in May.

Sonola agreed the headline inflation figures are distorting the real picture largely because energy has been so deflationary. Gas prices are down 26.5% in the past year, according to the latest consumer price index.

Meanwhile, housing prices are fueling core inflation while strong wage growth has led to sticky service industry prices. For instance, while food-at-home prices month-to-month are barely growing in 2023, food-away-from-home prices are climbing at much stronger clips.

“Unemployment below 4% is probably still going to bring about inflationary pressures on the wage front,” Sonola said. “As perverse as this sounds, the Fed will be happy to see unemployment in the 4% range, 4% to 4.5%, just so that takes away the pressure on wages.”

Tags: Consumer Price Index, Economy, Federal Reserve, Fitch Ratings, Inflation, Interest rates, Personal Consumption Expenditures, Recession, Unemployment rate

Simone Del Rosario:

Whatever happened to that recession? Now, I’m not asking for it. I’m just saying that several months ago, top economists predicted that we’d be in it right now. Instead, today, consumer confidence is at a two-year high. Unemployment is still well below 4%. And now the majority of business economists say the odds of a near-term recession, that is sometime in the next year, are 50% or less. Now we’ve got a huge week in business from the Fed to GDP to inflation numbers and then to those earnings. And we also have the head of US regional economics at Fitch ratings, Olu Sonola, here to break it all down for us. Olu, Fitch was among those predicting that we’d be in a recession at this time. Do you still predict that happening in the next year?

Olu Sonola:

We actually still, and thank you for having me, we still do have it on the cards. We actually, we pushed it forward to the end of the year. So we’re still looking at a very mild recession, I have to add, at the end of the fourth quarter into the first quarter of 2024. But the bottom line really is that this is a very resilient economy and the strength of the labor market has surprised everybody. And there’s a possibility that may actually continue, even though we think the labor markets would weaken from the third quarter going out through to 2024.

Simone Del Rosario:

So what sort of figures are you looking at if this is a mild recession? What does unemployment look like?

Olu Sonola:

We think unemployment will be in the 4% region by the end of the year because we think the labor market would weaken, particularly in the fourth quarter of the year. And we think, you know, ultimately we’ll top out in the 5% range, right about around 5% at the end of 2024. Given where we are, 3.6%, that may seem high, but I think the reality is that we think consumer spending will slow. towards the end of the year. I think income growth will also slow, giving higher unemployment towards the end of the year. We think we’ll see a weaker economy at the end of this year into next year.

Simone Del Rosario:

And of course, one of the biggest things is putting pressure on this economy right now is the Fed’s rate hike campaign. We’ve got a decision on Wednesday, seems all but assured they’re going to be raising that rate again. Is this it?

Olu Sonola:

It seems like it may be one and done, because inflation numbers have been surprisingly lower than expected. We’re at 3% now. Nobody actually thought we’d be at 3% this quickly, given where we are. And even the month on month is also cooperating. But I think the Fed will be paying a lot more attention to core inflation, which is still more than double its target. They tend to strip out, prefer stripping our energy and food. And core inflation now is very close to five. It’s still more than double their target. So as long as that’s still above three, I think you cannot completely rule out another hike. They’re probably going to be data driven over the next couple of months to see if that downward trajectory continues.

Simone Del Rosario:

And we’ve got the Fed’s preferred inflation gauge coming out at the end of this week. Despite the declines that we’ve been seeing in the headline, as you talked about, pretty significant declines in headline PCE and CPI, core PCE, that’s what the Fed says they love to look at, it hasn’t really budged at all in 2023. What does that tell us about inflation right now? And are these headline numbers kind of distorting the real picture?

Olu Sonola:

They are to a large extent because energy has been deflationary. So if we go this time last year, oil prices were about $120, gas prices were about $5. Now you’re talking oil prices in that 70 range and gas prices below 4%. So that’s 25%, 30% decline in those prices and that has fed through to CPI and even PCE. The bottom line is that PCE shelter is important. And that tends to lag. And also, super core, it’s so-called super core. Wages is also very, very important because what’s propping up core is the services component of things particularly. I think goods prices have been very, very cooperative, but services have been very, very sticky. And that’s typical. It takes a while for you to get inflation out of the services sector. But this last print that we saw on the CPI front actually bodes well for PCE. And I think the Fed would have been really, really happy with the last print and hope that continues for the next couple of months. If that actually continues for the next couple of months, then it’s very likely that tomorrow’s increase will probably be the last.

Simone Del Rosario:

Do you see that core inflation gets below 3% without a recession?

Olu Sonola:

So that’s a tough one. I think it’s possible, it’s feasible. I think it’s likely to happen. Now, the key downside risk really is the labor market. You have a really tight labor market. Unemployment below four is probably still going to bring about inflationary pressures on the wage front. So I think the Fed will be happy, and as perverse as this sounds, to be The Fed will be happy to see unemployment in the 4% range, 4% to 4.5%, just so that takes away the pressure on wages. And that can be long lasting because that’s the key. The key really is for us to have wage growth that’s below 4% or maybe around 3%. That’s really the wage growth that you need to have a 2%, a consistent 2% target.

Simone Del Rosario:

And if these figures go the way that you’re predicting at this moment, I know this is pretty far in the future, but when do you see the Fed possibly cutting rates?

Olu Sonola:

No, we are looking at the first, the tail end of the first quarter of next year. So basically March and maybe a little bit later than that. And, you know, at that point, we expect inflation to be definitely below three, somewhere between 2.5% and 3%. And if you have headline in that range and you also have core inflation, I’m talking CPI now, also right around 3%, then you actually are in a, good position to cut rates because you don’t want the real rate environment to be too contractionary. You don’t want that to be too restrictive. So if inflation comes down and it’s clear that it’s sustained, then yes, clearly the Fed will have to cut rates probably by the first end of the first quarter of next year.

Simone Del Rosario:

Olu Sonola of Fitch Ratings. Thank you so much.

Olu Sonola:

Thank you for having me.

Media Landscape

This story is a Media Miss by the left as only 30% of the coverage is from left leaning media.

Learn more about this dataLeft 30%

Center 30%

Right 40%

Bias Distribution

11 other sources covering this story

Total News Sources

11

Leaning Left

3

Center

3

Leaning Right

4

Last Updated

1 year ago

Bias Distribution Powered by Ground News™

MOST POPULAR

-

AP Images

AP Images

N. Korea hackers steal military secrets, hit Air Force bases, NASA, US says

-

Getty Images

Getty Images

A convicted child rapist is competing in Paris Games, many want to know why

-

AP

AP

Barack and Michelle Obama endorse Kamala Harris for president

-

Reuters

Reuters

Attacks disrupt trains ahead of Olympics opening ceremony