The nation’s budget is in constant triage. Congress again packed the wound by passing a temporary funding patch to keep the government’s lights on until early next year, but fiscally, the U.S. is still bleeding.

Download the SAN app today to stay up-to-date with Unbiased. Straight Facts™.

Point phone camera here

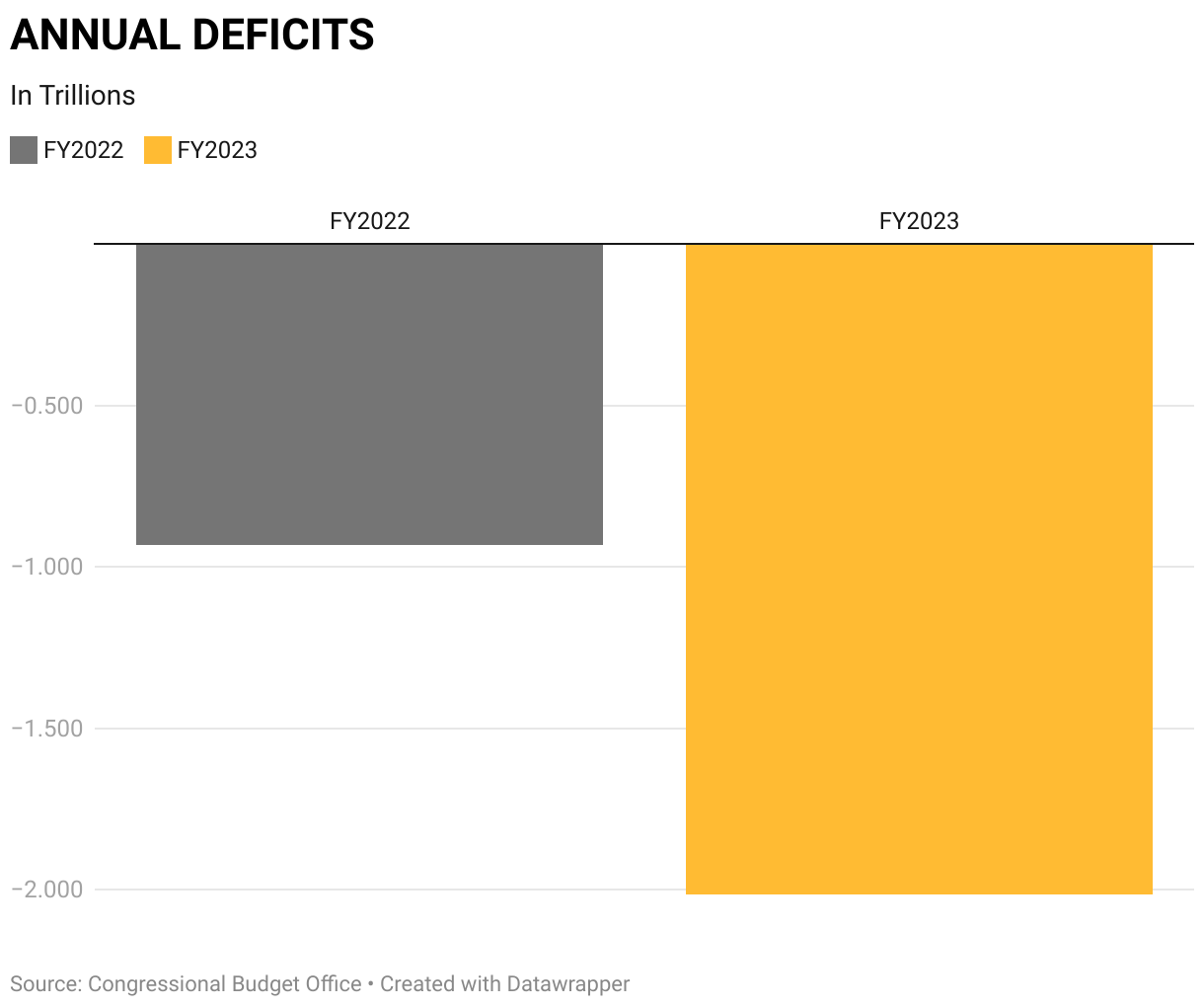

The federal deficit grew to $2 trillion in fiscal year 2023, double the prior year’s deficit, according to Congressional Budget Office (CBO) calculations when removing student loan cancellation, which the Supreme Court struck down in June.

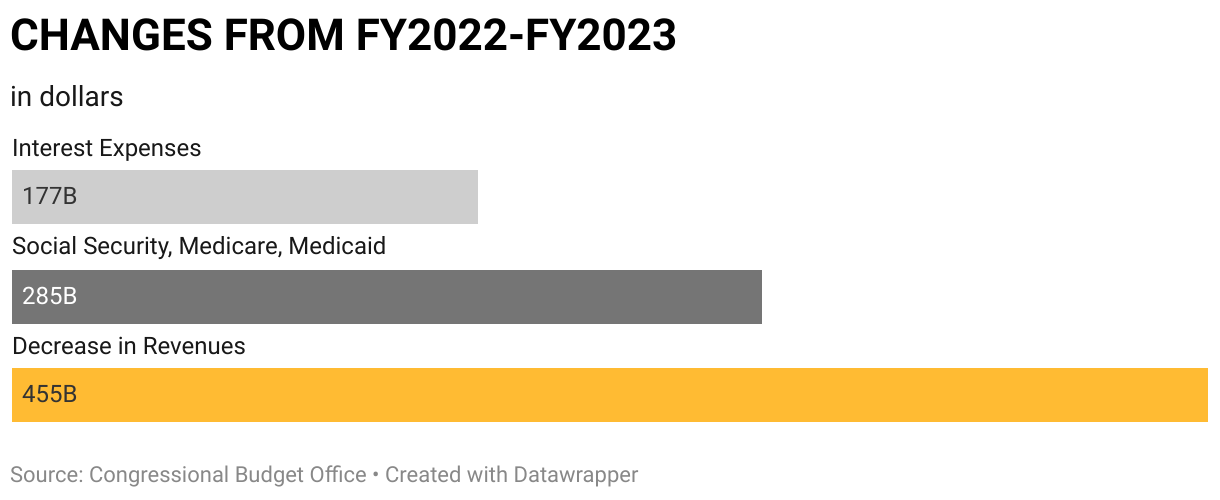

The ballooning deficit is due in large part to rising costs in interest payments, up 33% from last year; and Social Security, Medicare and Medicaid, up 11%. In addition, tax revenues declined in fiscal year 2023, bringing in 9% less than the previous year. So in two areas the CBO says could help tackle deficits, spending and taxes, both are going in the wrong direction.

Straight Arrow News spoke with CBO Director Phillip Swagel about the country’s financial outlook as Moody’s cut U.S. credit outlook to negative from stable.

This interview has been edited for clarity.

Simone Del Rosario: How concerned are you about the U.S. credit outlook going negative?

Phillip Swagel: I think about the U.S. fiscal situation at several horizons, so let’s think about the short term and the long term. The short term is what the credit agencies are looking at and saying, our fiscal situation is not just difficult, but we as a nation are having a difficult time dealing with it and making decisions about it, and they changed their outlook on that.

It looks like the Congress will now have until January and February 2024 to make decisions about funding the government. And at CBO, we’re here to support them, to support policymakers, as they do that. So that’s the short term.

The longer-term trajectory is what’s especially difficult. We have very high deficits, we have a rising debt stock, and it’s unusual to have this at a time when the economy is doing pretty decently. We’re past the negatives of the pandemic, the labor market is reasonably strong, and so there are lots of positives in the economy, and yet the deficit is super wide and the trajectory is difficult. So that’s what I think of the long term, is that problem is still there.

Simone Del Rosario: We’re now paying $1 trillion a year to service our debt due to high debt and rising interest rates. Is that sustainable or does the Federal Reserve need to rethink its inflation-fighting strategy?

Phillip Swagel: A real piece of the challenge is that both as interest rates have risen over the past couple of years and as the amount of debt has gone up, the net interest outlays – the carrying cost of the debt – has risen for the United States and it’s set to rise sharply over the next several years. That’s influenced in part by the Fed, but the U.S. Treasury securities, those interest rates are set in markets. The Fed generally sets the overnight rate and then the Treasury will borrow at 10-year, 20-year, 30-year and so on horizons.

So those are affected by lots of things and we’ve seen some volatility of those interest rates recently. They’ve fallen by multiple 10s of basis points in the last couple of weeks, but have risen very sharply over a year ago.

So the Fed is focused on inflation and focused on their mandate of maximum sustainable employment. The fiscal situation is affected by interest rates. And that’s one of the reasons why action is needed to tackle the fiscal situation. This is to make sure that all the other activities of the federal government are not swamped or pushed aside by the rising interest payments.

Simone Del Rosario: You’re calculating budget projections right now, right?

Phillip Swagel: We’re at the beginning of that process. So we put out our next 10-year budget outlook in February 2024. We’ll certainly do it before the statutory deadline of February 15. And we’re at the beginning of that process. We’re updating our economic forecast and then all of the budget analysts here at CBO will update their projections for every activity of the federal government. Then we’ll sum it up and release it in February.

Simone Del Rosario: How do you even do that with the volatility we’ve seen in interest rates? And what do those projections look like if these rates stay higher for longer?

Phillip Swagel: You put your finger on a key question and a key uncertainty in the outlook. We have to make a forecast and we have to do it basically now, within the next week, so that our budget analysts can do their work to update every account.

Just as an example, my colleague here who handles the SNAP – what used to be called food stamps – the projections of SNAP outlays depend on inflation and food prices. They depend on the state of the economy. If the unemployment rate is higher, then more people will sign up for benefits and so on. So we have to lock down the economics. But we won’t actually publish this until February.

So we know that there could be changes in the meantime, but we have to. And interest rates are a big part of that. Interest rates are volatile, but they’re also very meaningful for our budget projections. Let me just give you one example of that: Interest rates now are just under 4.5% as we’re talking here today. A year ago, when we did our last forecast, we thought the 10-year note would be at 3.8%. So that’s 70 basis points. Over 10 years, that’s an additional $2 trillion in interest costs. Interest rates are higher than we expected and that’s a massive change in the fiscal outlook.

Simone Del Rosario: The CBO acts as a nonpartisan body. You don’t give policy recommendations but you are there to help Congress out with what’s happening with the budget. You’ve given a series of options for tackling the country’s deficit. Could Congress accomplish what it needs to with the debt by either cutting spending alone or by raising revenues alone?

Phillip Swagel: Thank you for mentioning. In December 2022, at the end of the last Congress, we put out a report about options to reduce the federal budget deficit. And there’s a wide range, there’s changes in taxes, changes in spending. And as you said, CBO doesn’t say to Congress, do this or do that. We just provide analysis.

The challenge is that the fiscal situation is so difficult that to make the large changes needed, a wide range of options would have to be taken. So we put out a list of 17 large options, large in the sense of half a trillion dollars or more over 10 years – you know, real money, even to the federal government. Just to make the fiscal situation not get worse over the next 10 years, Congress would have to enact 10 of those. And each of them is very large and very difficult.

So that’s an indication of the scale of the problem. Could it be done by spending or revenue alone? Arithmetically, yes. I mean, it’s certainly possible and Congress, of course, can do whatever they want, we’re here to support them. So one could raise taxes by enough to narrow the budget deficit and stabilize the fiscal situation, or one could reduce spending by enough to do it. Those are just wrenching changes. And that’s the difficulty is that the fiscal situation is so difficult that really large changes are needed.

Simone Del Rosario: We’re in a 10-year window on Social Security. What happens if no hard choices are made in this arena by the time that window closes?

Phillip Swagel: This is the second driver of the fiscal situation. In the difficulty of the fiscal situation, we talked about interest rates before and rising net interest outlays. Then later in the 10-year budget window, the Social Security Trust Fund is exhausted in our projections. And so when that happens, the resources available to pay Social Security benefits are going to be about 25-27% less than the promises that have been made. There’s no provision in law to say what exactly happens, but Social Security will not have the statutory ability to pay the full promised benefits. That’s later, that’s in 2032 in our calculations, but that’s another driver of the need to make policy changes.

Simone Del Rosario: So what I’m hearing is that if no policy changes are made between now and then, beneficiaries would have their payments cut by 25%?

Phillip Swagel: That’s right. That would be under current law.

Simone Del Rosario: Legally, could the United States just take on more debt to fulfill those payments?

Phillip Swagel: That would take an act of Congress. The current law is what we analyzed. And again, we’re not saying that’s the right thing or the wrong thing. We’re not saying that Congress should do anything in particular or do nothing in particular, we provide an analysis of, under current law, what would happen. And the situation you just pointed at is certainly something policymakers could do. If they said, we don’t want to immediately raise taxes, we don’t want to immediately change benefits, let’s just have a transfer of funds from general revenue. That would mean that future generations would pay for the additional for the additional resources to make good on Social Security.

Simone Del Rosario: Okay, so for voters out there, either your members of Congress are doing something in the interim to make sure that those payments can be fulfilled in less than 10 years’ time, or they’re passing legislation to make sure they can take on more debt to fulfill those payments. Those things need to actually be done.

Phillip Swagel: Something has to be done. And then the latter option that you pointed to would essentially be saying people in the future will either get lower benefits or pay higher taxes. And since this is a generational issue, the current generation doesn’t bear the burden of the fiscal adjustment either through higher taxes or lower benefits than what’s been promised. A future generation will handle that. So it’s not like the problem goes away, it just gets deferred, and then the future generations would bear the burden.

Simone Del Rosario: This is something that people talk about a lot. Is it possible for us to just grow out of this problem?

Phillip Swagel: Well, growth would help, right, there are definitely things that can help. Stronger economic growth would mean more tax revenue: higher incomes, more revenues, more contributions into Social Security, and more resources to pay Medicare benefits as well and all the other things the federal government does. The challenge is that the benefits of Social Security would go up as well because the initial benefits that people receive are indexed to wages. When the economy is stronger, wages are higher and benefits are higher. So stronger growth helps, for sure it helps with Social Security, with Medicare, with the overall fiscal situation. It’s just that it would be very difficult for us to have strong enough economic growth for that alone to be the solution to the fiscal challenge.

Simone Del Rosario: The national debt, as we have these conversations right now, feels like a little bit of a boogeyman. We have huge amounts of debt and the interest payments that we’re paying on top of it are not helping because just compounding on itself. But overall, are government deficits a bad thing?

Phillip Swagel: It’s kind of interesting, it’s almost the same as for any of us as an individual. If we take out debt for an activity, it kind of depends on what it’s for. So the federal government borrowed and had more debt in response to the pandemic. And I’m not going to comment on every single individual piece of the response to the pandemic. But we supported households, we supported businesses, the U.S. had a relatively strong recovery from the pandemic. We developed the vaccines with considerable government support. It seems like that was a use of debt that – again, without going into the details of every single program, because obviously there’s a list of programs that didn’t work – on the whole, that was a fiscal response that was effective.

So that’s the challenge. If we’re going to borrow more, which we are under current law, what is it being used for and is that effective? And then just the last thought on this is who pays? Because eventually, some generation is going to pay, either through higher taxes or lower spending, lower benefits. It’s just a matter of which generation bears that burden.

Simone Del Rosario: So what do you say to people who advocate for continuing to take on more debt, saying, we don’t actually have to pay this back as long as we have buyers out in the world who will take it on?

Phillip Swagel: That’s one approach. It’s one that means an increasing risk that eventually, those buyers won’t be there, whether in the United States or around the world. Now, of course, the U.S. borrows in dollars, and we the federal government, the federal reserve, has the ability to create dollars. That’s what the Fed does. But in a sense, it means we won’t necessarily default on U.S. debt. But if the U.S. resorts to monetization to pay off that debt – which really no one is contemplating, I don’t think it would happen in the United States – that would lead to higher inflation, which we found out over the last couple of years has lots of negative consequences for American families. So being able to borrow is a good thing. It’s a strength of our economy, of our government, of our financial system. But there is a limit to it and eventually, adjustments need to be made.

Simone Del Rosario: What is that limit and when do those adjustments need to be made.

Phillip Swagel: That is really the difficult question. The U.S. government today has the ability to finance activities, both our existing activities under current law and new ones. If the U.S. government decides to undertake some new activity or new spending, social program, national security, tax relief; whatever the U.S. government wants to do, we as a nation have the ability to fund that. But at some point, that would be a challenge. The difficulty is that it depends on market participants’ beliefs, it depends on what’s going on in the rest of the world. So it’s difficult to identify, well, here is the moment at which, kind of the wily coyote moment, when we have a real problem. But more debt and continued deficits increases the risk of negative effects.

Tags: Debt ceiling, Deficit, Economy, Federal Funds Target Rate, Federal Reserve, GDP, Inflation, Interest rates, Jerome Powell, Jobs, Medicaid, Medicare, National Debt, Phillip Swagel, Recession, Snap, Social Security, Student Loans, Taxes, U.S. Congress, U.S. Congressional Budget Office, U.S. Dollar, U.S. Treasury Department

Simone Del Rosario: The nation’s budget is in constant triage, but no one’s taking the patient to surgery. Congress again packed the wound, passing a temporary funding patch to keep the government’s lights on until next year. But we’re still bleeding. The federal deficit grew to $2 trillion in fiscal year 2023, double the prior year’s deficit. That’s thanks in large part to double-digit percentage increases in interest payments, Medicare and Social Security, while tax collections took a dive. So in two areas that could help tackle deficits, spending and taxes, they’re both going in the wrong direction. Joining me is Phillip Swagel, director of the Congressional Budget Office. Credit rating agencies obviously don’t think this isn’t a big deal. Moody’s is the latest to cut its current US credit outlook. Of course, we know that Fitch already downgraded the US credit rating earlier this year. How concerned are you about this independent view of the US’s finances?

Phillip Swagel: Simone, thanks very much. You know, I think about the US fiscal situation at several horizons. And so when we think about the short term in the long term. In the short term is what, you know, the credit agencies are looking at, and saying that, you know, our fiscal situation is not just difficult but we as a nation are having a difficult time dealing with it, making decisions about it. And, you know, the downgrade, downgraded or, you know, changed their outlook on that. You know, it looks like the Congress will now have till January and February 2024, to make decisions about funding the government. And at CBO, we’re here to support them, to support policymakers, as they do that. So that’s kind of the short term. The longer term trajectory is what’s especially difficult. We have very high deficits, we have a rising debt stock. And it’s unusual to have this in a time when the economy is doing pretty decently, right. We’re past the negatives of the pandemic, the labor market is reasonably strong. And so there’s lots of positives in the economy, and yet the deficit is super wide and the trajectory is difficult. So that’s what I think of the long term is that problem is still there.

Simone Del Rosario: We’re now paying a trillion dollars a year to service our debt. Is that sustainable? Or does the Fed need to rethink its inflation-fighting strategy at this point?

Phillip Swagel: So a real piece of the challenge is that both as interest rates have risen over the past couple of years and as the amount of debt has gone up, the net interest outlays, so in some sense, the carrying cost of the debt, has risen for the United States, and it’s set to rise sharply over the next several years. That’s influenced in part by the Fed, but the US Treasury securities, those interest rates are set in markets, where the Fed generally sets the overnight rate and then the Treasury will borrow a 10 year, 20 year, 30 year and so on horizons. So those are affected by lots of things. And we’ve seen some volatility of those interest rates recently. They’ve fallen by multiple 10s of basis points in the last couple of weeks, but have risen very sharply over a year ago. So the Fed is focused on inflation and focused on their mandate of maximum sustainable employment. The fiscal situation is affected by interest rates. And that’s why action is needed, is one of the reasons why action is needed to tackle the fiscal situation. This is to make sure that all the other activities of the federal government are not swamped or pushed aside by the rising interest payments.

Simone Del Rosario: You’re calculating budget projections right now, right?

Phillip Swagel: We’re at the beginning of that process. So we put out our next 10 year budget outlook in February of 2024. We’ll certainly do it before the statutory deadline of February 15. And we’re at the beginning of that process, we’re updating our economic forecast. And then all of the budget analysts here at CBO will then update their projections for every activity of the federal government. And then we’ll sum it up and release it in February.

Simone Del Rosario: How do you even do that with the volatility we’ve seen in interest rates? And what do those projections look like if these rates stay higher for longer?

Phillip Swagel: Now, you put your finger on really a key question, and a key uncertainty in the outlook. So we have to make a forecast and we have to do it basically now, within the next week, so that our budget analysts can do their work to update every account, right? So just as an example, that analyst, my colleague here who handles the SNAP, what used to be called food stamps, right? The projections of SNAP outlays depend on inflation and food prices. They depend on the state of the economy. If the unemployment rate is higher, well then more people will sign up for benefits and so on. So we have to lock down the economics. But we won’t actually publish this until February. So we know that there could be changes in the meantime, but we have to. And interest rates are a big part of that. Interest rates are volatile, but they’re also very meaningful for our budget projections. Let me just give you one example that. Interest rates now are just under four and a half percent as we’re talking here today. A year ago, when we did our last forecast, we thought the 10 year note would be at 3.8. So that’s 70 basis points. Over 10 years, that’s an additional $2 trillion in interest costs. So it’s a massive, right, interest rates are higher than we expected. And that’s a massive change in the fiscal outlook.

Simone Del Rosario: Yeah, let me lay the scene here a little bit for our listeners right now. Obviously, as the director of the CBO, you all act as a nonpartisan body. You don’t give policy recommendations, but you are there to kind of help Congress out with what’s happening with the budget. You’ve given a series of options for tackling the country’s deficit. Could you accomplish what you need to by either cutting spending alone or by raising revenues alone?

Phillip Swagel: Thank you for mentioning, the report we did that you mentioned was December 2022. So at the end of the last Congress, we put out a report about options to reduce the federal budget deficit. And there’s a wide range, there’s changes in taxes, changes in spending. And as you said, CBO doesn’t say to Congress do this or do that. We just provide analysis. And the challenge is that the fiscal situation is so difficult that to make the large changes needed, a wide range of options would have to be taken. So we put out a list of 17 large options, so large in the sense of half a trillion dollars or more over 10 years. You know, real money, even the federal government. Just to make the fiscal situation not get worse over the next 10 years, Congress would have to enact 10 of those. And you know, each of them is very large and very difficult. And so that’s, you know, that’s really an indication of the scale of the problem. Could it be done by spending or revenue alone? You know, arithmetically? Yes. Right. I mean, it’s certainly possible and Congress, you know, of course, can do whatever they want, we’re here to support them. So one could raise taxes by enough to narrow the budget deficit, stabilize the fiscal situation, or one could reduce spending by enough to do it. Those are just wrenching changes. And that’s the difficulties of the fiscal situation is so difficult, that really large changes are needed.

Simone Del Rosario: Okay, so we’re in a 10-year window on Social Security. What happens if no hard choices are made in this arena by the time that window closes?

Phillip Swagel: No, thank you. This is the second driver of the fiscal situation. In the difficulty of the fiscal situation, we talked about interest rates before and rising net interest outlays. Then later in the 10 year budget window, the Social Security Trust Fund is exhausted in our projections. And so when that happens, the resources available to pay Social Security benefits are going to be about 25, 27% less than the promises that have been made. So there’s no provision in law to say, well what exactly happens, but Social Security will not have the statutory ability to pay the full promised benefits. And that’s insufficient. Look, this is later, this in 2032, in our calculations, but that’s another driver of the need to make policy changes.

Simone Del Rosario: So what I’m hearing is that if no policy changes are made between now and then, beneficiaries would have their payments cut by 20, 25%.

Phillip Swagel: That’s right. That would be under current law.

Simone Del Rosario: Legally, could the United States just take on more debt in order to fulfill those payments?

Phillip Swagel: That would take an act of Congress. Right. So the current law is what we analyzed. And again, we’re not saying that’s the right thing or the wrong thing. We’re not saying that Congress should do anything in particular or do nothing in particular, we provide an analysis of, under current law, what would happen. And in the situation you just pointed at, is certainly something policymakers could do. If they said, we don’t want to immediately raise taxes, we don’t want to immediately change benefits. Well, let’s just have a transfer of funds from general revenue. And that would mean that future generations, then, would pay for the additional for the additional resources to make good on Social Security.

Simone Del Rosario: Okay, so for voters out there, either your members of Congress are doing something in the interim to make sure that those payments can be fulfilled in less than 10 years time, or they’re passing legislation to make sure they can take on more debt to fulfill those payments, like those things need to actually be done.

Phillip Swagel: Something has to be done. And then the latter option that you pointed to would essentially be saying people in the future will either get lower benefits or pay higher taxes. Right, and since this is a generational issue, the current generation doesn’t bear the burden of the fiscal adjustment, again either through higher taxes or lower benefits than what’s been promised. A future generation will handle that. So it’s not like the problem goes away, it just gets deferred, and then the future generations would bear the burden.

Simone Del Rosario: This is something that people will talk about a lot. Is it possible for us to just grow out of this problem?

Phillip Swagel: Well, growth would help, right, there’s definitely things that can help. So stronger economic growth would mean more tax revenue, higher incomes, more revenues, more contributions into Social Security, and more resources to pay Medicare benefits as well and all the other things the federal government does. The challenge is that the benefits of social security would go up as well, right, because the initial benefits that people receive are indexed to wages. And so when the economy is stronger, wages are higher and benefits are higher. So stronger growth helps, for sure it helps with Social Security, with Medicare, with the overall fiscal situation, it’s just it would be very difficult for us to have strong enough economic growth, for that alone to be the solution to the fiscal challenge.

Simone Del Rosario: Now, obviously, the national debt, as we have these conversations right now, it feels like a little bit of a boogeyman, right. I mean, huge amounts of debt and, of course, the interest payments that we’re paying on top of it is not helping because just compounding on itself. But overall, are government deficits, are they a bad thing?

Phillip Swagel: Ah, you know, I mean, it’s kind of interesting. It’s like, almost the same as for any of us as an individual. If we take out debt for an activity, it kind of depends on what it’s for. So the federal government borrowed and had more debt in response to the pandemic. And I’m not going to comment on every single individual piece of the response to the pandemic. But we supported households, we supported businesses, the US had a relatively strong recovery from the pandemic, we develop the vaccines with considerable government support. It seems like that was, you know, a use of debt that, again, without going into the details of every single program, because obviously, there’s a list of programs that didn’t work, you know, on the whole, that was a fiscal response that was effective. And so that’s the challenge is, if we’re going to borrow more, which we are under current law, is what is it being used for, is that effective. And then just the last thought on this is who pays because eventually, some generation is going to pay, again, either through higher taxes or lower spending, lower benefits, it’s just a matter of which generation bears that burden.

Simone Del Rosario: So what do you say to people who advocate for just continuing to take on more debt, saying, we don’t actually have to pay this back as long as we have buyers out in the world who will take it on?

Phillip Swagel: That’s one approach, it’s one that means in increasing risk, that eventually, those buyers won’t be there, whether in in the United States or around the world. Now, of course, the US borrows in dollars. And we the federal government, the federal reserve, has the ability to create dollars, right. That’s what the Fed does. But in a sense, it means we won’t necessarily default on US debt. But if the US resorts to monetization, to pay off that debt, which really no one is contemplating. No one is contemplating. I don’t think it would happen in the United States. But that would lead to higher inflation, which we found out over the last couple of years has lots of negative consequences for American families. So, you know, being able to borrow is a good thing. It’s a strength of our economy, of our government, of our financial system. But there is a limit to it, and eventually, adjustments need to be made.

Simone Del Rosario: Okay. And we all want to know what that limit is, and when those adjustments need to be made.

Phillip Swagel: That, you know, that is really the, I’m leaning back in my chair. That is really the difficult question. Yeah, the US government today, you know, has the ability to finance activities, you know, both our existing activities under current law, and new ones. If the US government decides to undertake some new activity, or new spending, you know, social program, national security, tax relief, whatever the US government wants to do, we as a nation have the ability to fund that. But at some point, that would be a challenge. And then the difficulty is that it depends on market participants’ beliefs, it depends on what’s going on in the rest of the world. So it’s difficult to identify, well, here is the moment at which, you know, kind of the wily coyote moment when we have a real problem, but more debt, continued deficits, increases the risk of negative effects.

Simone Del Rosario: Alright, we’re gonna leave it there. Phill Swagel, director of the Congressional Budget Office. Thank you so much for your time today.

Phillip Swagel: Simone, thanks so much, it’s really a pleasure.

MOST POPULAR

-

Getty Images

Getty Images

Pythons decimate Florida’s wildlife, is eating them the answer?

-

Getty Images

Getty Images

Trump could lose Secret Service protection if found guilty

-

AP Images

AP Images

Argentina asks to join NATO as Milei looks to enhance security, strengthen ties

-

Getty Images

Getty Images

Utah students protest 'furries,' school admin deny problem