It’s not anecdotal: Extreme natural disasters are happening more often and causing way more damage. Insurance is supposed to be there to safeguard homeowners in case the worst happens to their property. However, in disaster-prone areas, some insurers are declaring that it’s too risky to keep doing business there.

Download the SAN app today to stay up-to-date with Unbiased. Straight Facts™.

Point phone camera here

“The last few years, insurers have lost money,” said Scott Holeman, a spokesperson for the Insurance Information Institute, known as Triple-I.

“If the combined ratio is under 100, insurance companies can make money,” Holeman explained. “If that combined ratio is over 100, that means they’re paying out more money than they’re taking in. And that’s not sustainable for any business to pay out more than what you’re collecting.”

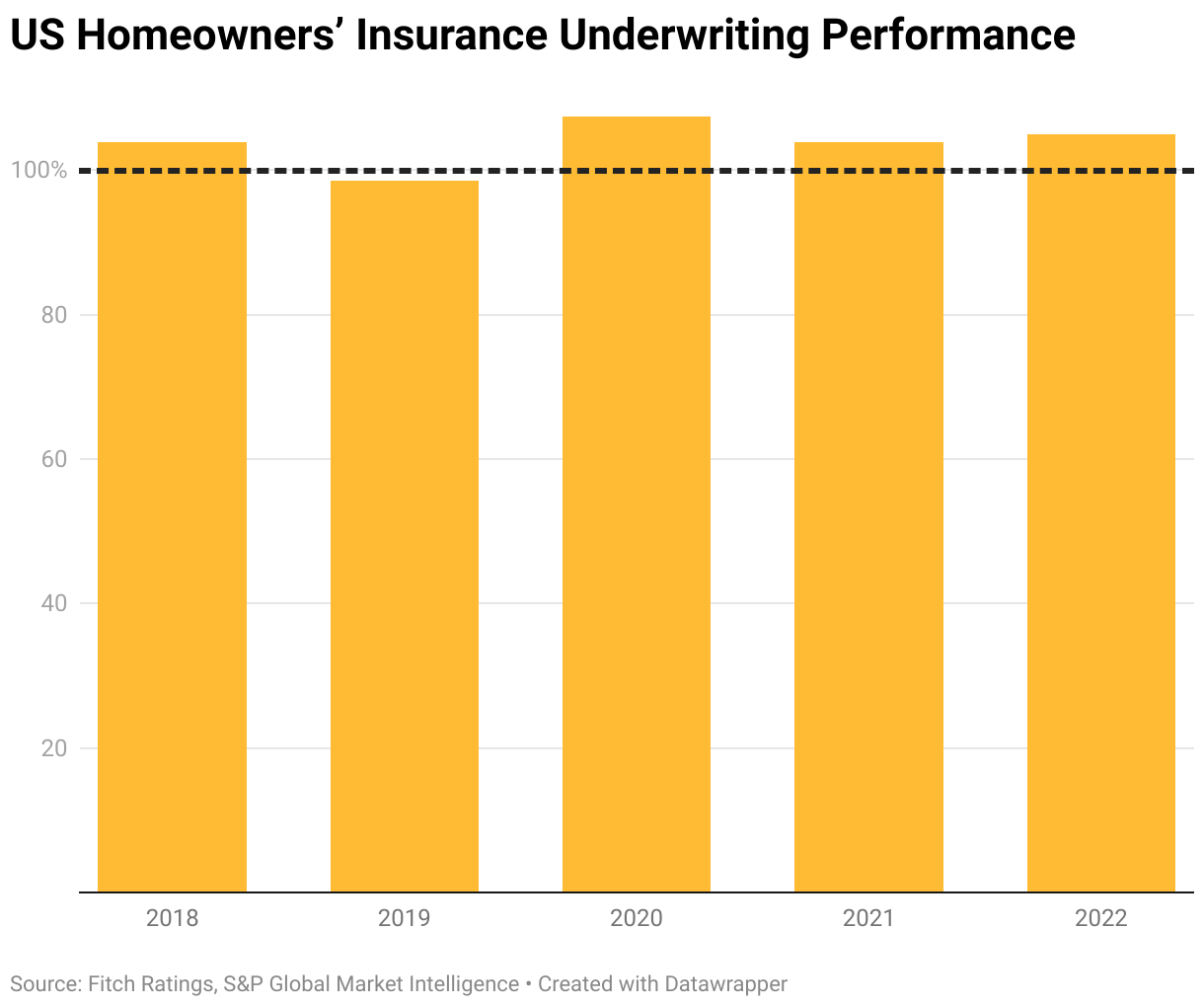

For four out of the past five years, national data shows homeowners’ insurers have earned less in premiums than they’ve paid out in losses and expenses. Taking a closer look at markets like Florida and California, it’s no wonder insurers are jumping ship.

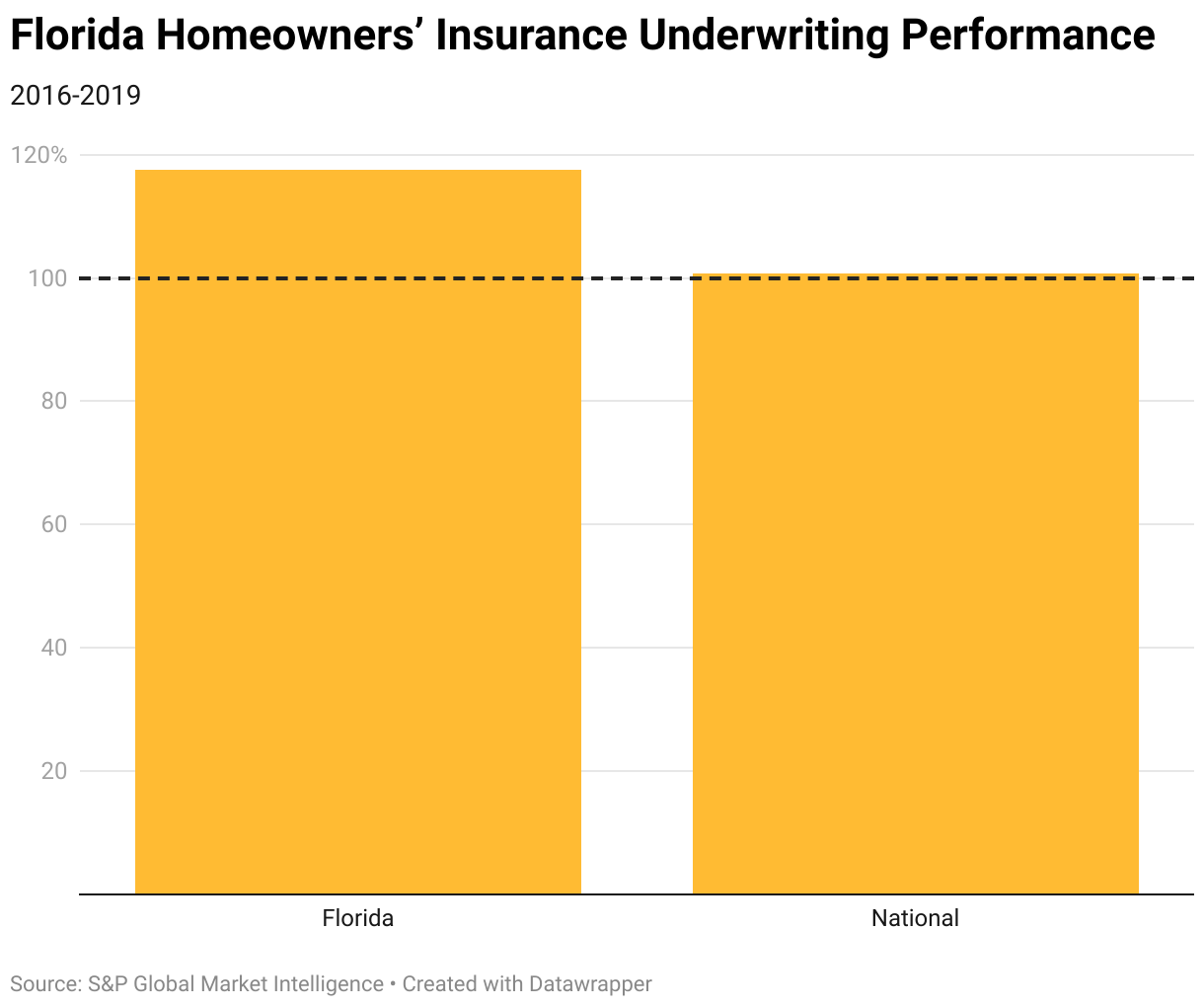

From 2016-2019, for every $100 in premiums Florida home insurers received, they paid out $117.50 in losses and expenses. On a national level, it was basically break-even over that time at $100.70.

Insurers are going to have to raise rates to stay in business or leave the market.

Scott Holeman, Insurance Information Institute spokesperson

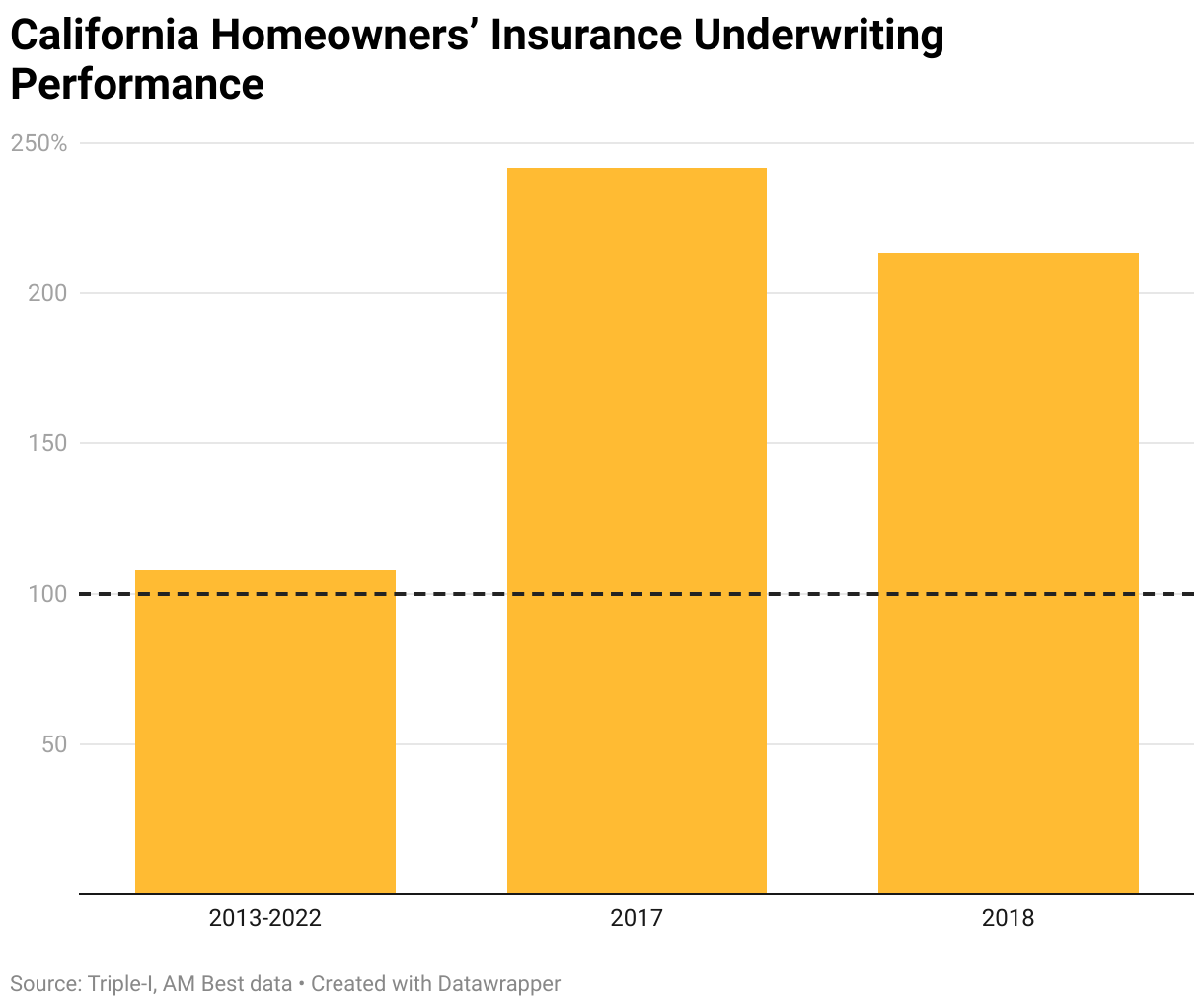

Meanwhile, California insurers are still catching up from the fateful fire seasons of 2017 and 2018. Triple-I said that in the last decade, California insurers made healthy profits in the homeowners’ insurance business for eight out of 10 years. However, the combined ratio is still 108.1% over that time. That’s because for every $100 in premiums received, California’s home insurers paid out $241.90 in 2017 and $213.40 in 2018.

This year the state’s largest insurer, State Farm, said it would stop selling new home policies in the state. Allstate had quietly stopped selling them last year and announced the move after State Farm. Others have followed suit. Farmers has also significantly pulled back in Florida and California.

“Florida and California are seeing a lot of issues but it’s not just there — we’re seeing places like Arkansas and Mississippi were hit by tornadoes earlier this year,” Holeman said. “Insurers are going to have to raise rates to stay in business or leave the market.”

This is part 1 of a 3-part series on the homeowners’ insurance crisis. Watch part 2: With home insurance premiums through the roof, some homeowners go ‘naked’; and part 3: Fueling home insurance crisis: Natural disasters rack up billions in damage.

Tags: California, Farmers Insurance, Florida, Home insurance, Insurance, natural disaster, premium, State Farm, Wildfire

SIMONE DEL ROSARIO: It’s not anecdotal. Extreme natural disasters are happening more often and causing way more damage. Insurance is supposed to be there to cover you in case the worst happens to your home. But in disaster prone areas, some insurers are saying it’s just too risky to keep doing business there.

SCOTT HOLEMAN: The last few years, insurers have lost money.

SIMONE DEL ROSARIO: Scott Holeman is a spokesperson for Triple-I, Insurance Information Institute.

SCOTT HOLEMAN: If the combined ratio is under 100, insurance companies can make money. If that combined ratio is over 100, that means they’re paying out more money than they’re taking in. And that’s not sustainable for any business to pay out more than what you’re collecting.

SIMONE DEL ROSARIO: Look closer at markets like Florida and California, and it’s no wonder insurers are jumping ship. From 2016-2019, for every $100 in premiums Florida insurers received, they paid out $117.50 in losses and expenses. While on a national level, it was basically break even over that time.

Meanwhile, California insurers are still catching up from the fateful fire seasons of 2017 and 2018. Triple-I says in the last decade, California insurers made healthy profits in the homeowners’ insurance business for 8 out of 10 years. But the combined ratio is still 108.1% over that time. That’s because for every $100 in premiums received, California’s home insurers paid out $241.90 in 2017 and $213.40 in 2018.

This year the state’s largest insurer, State Farm, said it would stop selling new home policies in the state. Allstate had quietly stopped selling them last year. Others have followed suit. Farmers has also pulled back in Florida and California.

SCOTT HOLEMAN: Florida and California are seeing a lot of issues. But it’s not just there, we’re seeing places like Arkansas and Mississippi were hit by tornadoes earlier this year. Insurers are going to have to raise rates to stay in business or leave the market.

SIMONE DEL ROSARIO: This is part 1 of a 3-part series on the homeowners’ insurance crisis. Be sure to download the SAN app and enable notifications so you can catch part 2 on skyrocketing premiums coming soon.

MOST POPULAR

-

Getty Images

Getty Images

Texas Gov. Abbott warns migrants of alligators in Rio Grande

-

Reuters

Reuters

China permanently deploys warships to second overseas base

-

Getty Images

Getty Images

Harvey Weinstein’s rape conviction overturned, victims could see new trial

-

Al-Qassam Brigades

Al-Qassam Brigades

Hamas video shows American hostage with arm amputated