When the worst happens to your home, a common consolation is, “That is what insurance is for.” But with the price of homeowners’ insurance going through the roof, more people are opting to go without.

About 12% of homeowners do not carry homeowners’ insurance, according to a recent Insurance Information Institute (Triple-I) analysis. Nearly half of those households make less than $40,000 per year.

Download the SAN app today to stay up-to-date with Unbiased. Straight Facts™.

Point phone camera here

Mortgage lenders require owners to have insurance, so those who don’t have insurance likely own their property outright.

“For some people, they may want to walk away and move to another location, but just know, you’re gonna lose everything,” Triple-I spokesperson Scott Holeman said.

Some are deciding it’s a price they’d have to pay when they can’t afford to pay their premiums.

This is part 2 of a 3-part series on the homeowners’ insurance crisis. Watch part 1: Why more insurers are refusing to provide home insurance; and part 3: Fueling home insurance crisis: Natural disasters rack up billions in damage.

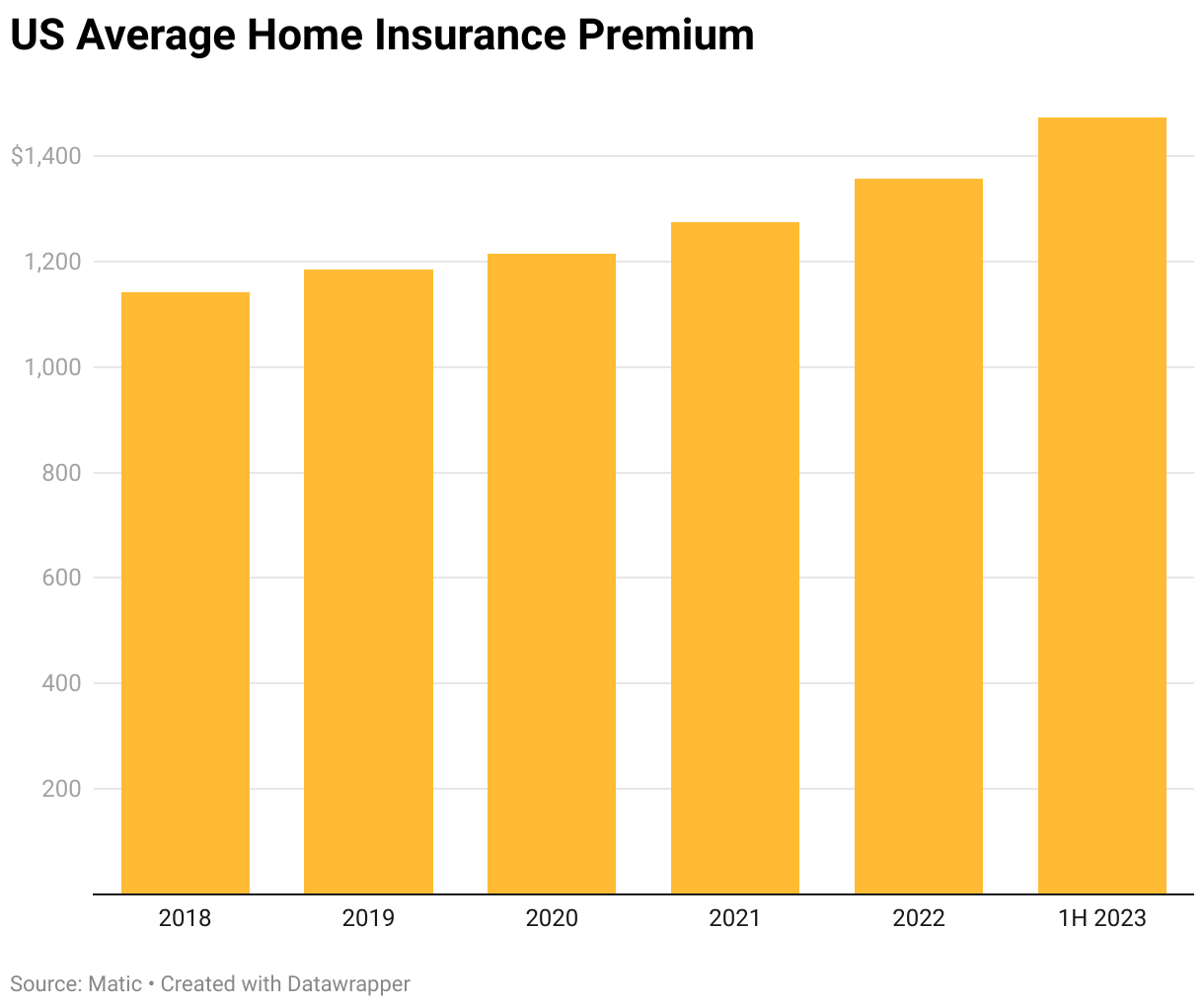

Nationally, the average premium has gone up nearly 30% since 2018, according to Matic. Most of the increase is attributed to the rising cost of repairs and extreme natural disasters.

But many states have it even worse. In Nebraska, $300,000 in dwelling coverage costs more than $3,500 per year, double the national average. That’s second only to Oklahoma.

“It’s either the price goes up so high people can’t afford it, or the companies go out of business, and no one can be insured,” Holeman said.

It’s a problem in places like California, where average premiums are below the national average. Recently, insurers have lost so much money in the state that State Farm, Allstate, Farmers, and USAA have paused or are limiting new coverage. Together, those four make up nearly a quarter of California’s property insurance market share.

“There are a lot of policy decisions that are going to have to be made in some of those high-risk states, and they are having [those discussions],” Holeman said.

State governments regulate how much insurers can charge, and 31 states have approved double-digit rate increases since the start of 2022, according to a Wall Street Journal analysis of S&P Global data.

Facing an insurance exodus in California, the state’s chief regulator just ruled insurers can now factor in future risks when setting prices, something many other states already allow. The state agency said eight insurance companies have requested rate increases of at least 20% or higher this year.

“Insurance is about spreading risk; it’s about managing risk; and it’s about assessing that risk to know what to charge people,” Holeman said. “And as we see conditions changing and more people living in those risky areas, there are more people exposed.”

This is part 2 of a 3-part series on the homeowners’ insurance crisis. Watch part 1: Why more insurers are refusing to provide home insurance; and part 3: Fueling home insurance crisis: Natural disasters rack up billions in damage.

SIMONE DEL ROSARIO: When the worst happens to your home, a common consolation is: that is what insurance is for. But with the price of homeowners’ insurance going through the roof, more people are opting to go without.

SCOTT HOLEMAN: That’s really sad. And it’s really unwise.

SIMONE DEL ROSARIO: Scott Holeman is a spokesperson for Triple-I, Insurance Information Institute. Their analysis found 12% of homeowners do not carry homeowners’ insurance. About half of those households make less than $40,000 per year.

SCOTT HOLEMAN: For some people, they may want to walk away and move to another location, but just know, you’re gonna lose everything.

SIMONE DEL ROSARIO: Some are deciding it’s a price they’d have to pay, when they can’t afford to pay their premiums. Nationally, the average premium has gone up nearly 30% since 2018, mostly attributed to the rising cost of repairs and extreme natural disasters. But many states have it even worse. In Nebraska, $300,000 in dwelling coverage costs more than $3,500 per year, double the national average. That’s second only to Oklahoma.

SCOTT HOLEMAN: It’s either the price goes up so high people can’t afford it or the companies go out of business and no one can be insured.

SIMONE DEL ROSARIO: It’s a problem in places like California, where average premiums are below the national average. Recently insurers have lost so much money in the state that nearly a quarter of the market share is either stopping or limiting new coverage.

SCOTT HOLEMAN: There are a lot of policy decisions that are going to have to be made in some of those high risk states and they are having them.

SIMONE DEL ROSARIO: State governments regulate how much insurers can charge. And 31 states have approved double-digit rate increases since the start of 2022, according to a Wall Street Journal analysis of S&P Global data. Facing an insurance exodus in California, the state’s chief regulator just ruled insurers can now factor in future risks when setting prices, something many other states already allow. The state agency said eight insurance companies have requested rate increases of at least 20% or higher this year.

SCOTT HOLEMAN: Insurance is about spreading risk. It’s about managing risk. And it’s about assessing that risk to to know what to charge people. And as we see conditions changing and more people living in those risky areas, there are more people exposed.

SIMONE DEL ROSARIO: This is part 2 of a 3-part series on the homeowners’ insurance crisis. Be sure to download the SAN app and enable notifications so you can catch part 3 on billion-dollar natural disasters coming soon. And search SAN for part 1 on why more insurers are refusing to provide home insurance.

MOST POPULAR

-

Getty Images

Getty Images

Texas Gov. Abbott warns migrants of alligators in Rio Grande

-

Reuters

Reuters

China permanently deploys warships to second overseas base

-

Getty Images

Getty Images

Harvey Weinstein’s rape conviction overturned, victims could see new trial

-

Al-Qassam Brigades

Al-Qassam Brigades

Hamas video shows American hostage with arm amputated