The creator of a recession indicator that was triggered this past week said her rule is broken this time around and there’s no recession right now. But not everyone agrees. In fact, a different recession indicator points to the U.S. having entered a recession in October of last year.

“We’re not in a recession,” Sahm Rule creator Claudia Sahm told Straight Arrow News. “It’s never time to panic, but it’s also not recession time either. So it’s not a recession. And yet the risks are there.”

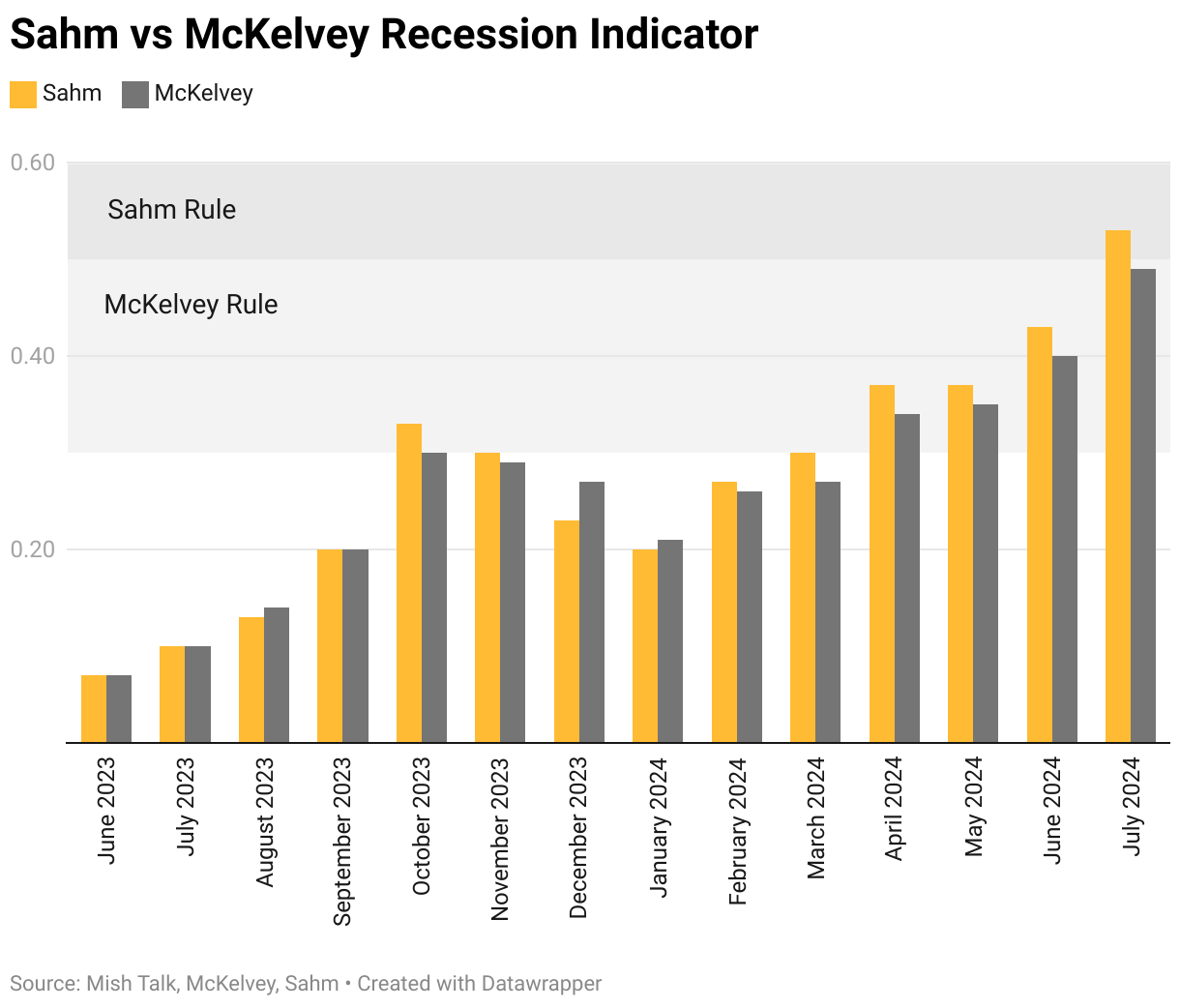

Recessions are declared by the National Bureau of Economic Research in hindsight by looking at the economy’s growth over previous quarters. Recession indicators like Sahm’s look at rising unemployment rate trends for more immediate indications the country has entered a recession.

Point phone camera here

While Sahm’s rule was triggered by last week’s release of July’s jobs data, a different recession indicator was set off last October. In simple terms, the McKelvey Rule hits when the three-month average rise in unemployment hits 0.3 percentage points above the year’s low, compared to Sahm’s 0.5-percentage-point threshold.

That’s one reason why former Federal Reserve adviser and current CEO of QI Research Danielle DiMartino Booth says we are already in a recession.

The following transcript has been edited for length and clarity. Watch the full interview in the video above.

Danielle DiMartino Booth: I do think we’re in recession. Everything that we’ve seen from the Bureau of Labor Statistics with regards to the fourth quarter of 2023 indicates that they’re going to be revising into negative territory the final three months of 2023.

So that would stretch job losses from the third quarter of 2023 – when there were 192,000 jobs lost in the United States – that would stretch that into the fourth quarter and give us a six-month stretch of job losses upon revising the Bureau of Labor Statistics survey data with the hard data that we get from the Census Bureau, where companies are legally obligated once a quarter to report their headcount.

And that’s kind of the ultimate decision. That’s when the ink dries, if you will, on the payrolls data that we see the Bureau of Labor Statistics release.

Simone Del Rosario: So we’re looking at a recession that would have started in October of last year?

Danielle DiMartino Booth: I personally see the recession as having started in October 2023 because that’s the first time that the McKelvey Rule, which is less arduous than the Sahm Rule – and it doesn’t date back to 1948, it dates back to 1968 – but it has not missed a single recession since then.

Rather than a 0.5-percentage-point increase in the unemployment rate off of its lowest level in the prior 12 months, it is a 0.3-percentage-point increase in the unemployment rate over the prior 12-month period’s low.

Again, it has a spotless track record since 1968. It was triggered in October of 2023. The Bureau of Labor Statistics said that we lost 192,000 jobs in the three months ending Sept. 30, 2023. So the National Bureau of Economic Research could theoretically backdate it further, but again, the McKelvey Rule is what I’ve relied on.

The former chief economist at Goldman Sachs, he was interviewed by the Wall Street Journal in January 2008 when his rule was triggered, and he was asked the same question: ‘Well, your McKelvey Rule was triggered in December of 2007. Do you think we’re in recession?’ And he said, ‘Well, you know, my rule might be broken,’ basically.

But of course, the NBER did backdate that recession to December 2007 and the McKelvey Rule was not broken. Luckily, the Bloomberg Economics team agrees with me that recession, that job losses started in October 2023.

Simone Del Rosario: Why isn’t the Federal Reserve looking at these data points?

Danielle DiMartino Booth: I think the Fed is choosing to look the other way in this instance. There are some regulations that the Fed has been working on that could really define Chair Powell’s legacy – that would begin to regulate the private equities, the hedge funds, the BlackRocks of the world that are in some cases larger than banks if you consider the trillions of dollars that they have under management – and in order to push through with some of these regulations, he really does need higher-for-longer [rates] on his side.

He needs the higher-for-longer policy enough to go with what the Bureau of Labor Statistics first reports, even though we know that since January 2023, we’ve seen one downward revision after another to the data. It’s become systematic, in fact, the persistence with which we’ve seen downward revisions to what’s first reported. But again, I think [Fed Chair Jerome] Powell’s got his own reasons.

Simone Del Rosario: How do you square this idea that we could be in a recession right now with the GDP numbers that we’re seeing? The latest reading, the advance estimate, showed an annual growth rate of 2.8%.

Danielle DiMartino Booth: So we had 2-point-something percent in 2001 when it was first reported. Of course, it was another six quarters later that we revised it and found out that it was a negative number.

It takes magnitudes of the amount of time to get correct unemployment data, correct payrolls data. You can double the time that it takes to figure out what the actual GDP is that’s associated with that time frame.

If you find out that you’re 830,000 jobs shy of what you thought you were, which is what we found out in the third quarter of 2023 looking backward with hard data in hand, then you have to subsequently go back and back out. Well, 830,000 people were not actually working; 830,000 people were not actually producing the economic output that we thought we were. So you’ve got to back that out.

It takes a lot of time for the Bureau of Labor Statistics data to work its way into subsequent revisions for the Bureau of Economic Analysis data, for GDP.

It’s at inflection points. It’s when contractions become expansions, when expansions become contractions, that these big statistical agencies have trouble seeing the turning point, given their modeling.

But it wasn’t until 2018 that we saw the final GDP revision from the Great Recession that ended in June 2009. Again, the recession ended June 2009. We didn’t get the final revision for GDP for that recession until 2018.

Simone Del Rosario: On one hand, this can seem incredibly frustrating if people feel like we’re in a recession, they feel like the economy’s not good, and yet we continue to get, on the surface, economic releases that show a pretty strong economy. But that said, if, to your point, we are already in a recession, does that take some of the panic away since we’ve already been going through it, or is it going to get worse? What’s your read on that?

Danielle DiMartino Booth: Well, your average recession is 10 months long in the post-war era. So using that average length of time, we should theoretically be starting to recover and coming out of recession.

That being said, the Federal Reserve has waited now 12 months, now longer than 12 months, and the longer it waits, typically the deeper and longer the recession is as a result.

There have been some great studies that empirically demonstrate this. The period leading up to the Great Recession, 2007-2009, the Fed waited 15 months. It’s the longest the Fed’s ever waited.

So we’re just at the 12-month mark now. But it certainly looks like we’re going to get to the 14-month mark if it’s Sept. 18 that we can anticipate that first rate cut. So that’s about as long as the Fed has ever waited to provide relief in the form of the beginning of an easing cycle.

Tags: Bureau of Labor Statistics, Census, Consumer Confidence, Danielle DiMartino Booth, Economy, Federal Reserve, Great Recession, Jerome Powell, Jobs, National Bureau of Economic Research, Recession, U.S. Census Bureau, U.S. Economy, Unemployment rate

Claudia Sahm: We’re not in a recession. I mean, it’s never time to panic, but it’s also not recession time either. So it’s not a recession. And yet the risks are there.

Simone Del Rosario:

Recession has been on the lips of every economy-focused American for the last week, and the conversation could get even more heated next week as we finally get a look at July’s inflation data.

Economist and creator of the Sahm Rule Claudia Sahm says we aren’t in a recession quite yet, despite her nearly pristine indicator being triggered after last Friday’s jobs report.

But when it comes to economic theory, someone else will always have a differing opinion. Enter our next guest and friend Danielle DiMartino Booth, CEO of QI Research and former Fed advisor. Danielle says the U.S. could be in a “plain vanilla recession.”

Danielle, I am afraid that in my adult life, I don’t even know what that is.

Danielle DiMartino Booth:

Well, okay, I’m gonna have to declare innocence here because I did not write that headline. So, at all. I do think we’re in recession.

Everything that we’ve seen from the Bureau of Labor Statistics with regards to the fourth quarter of 2023 indicates that they’re going to be revising into negative territory the final three months of 2023. So that would stretch job losses from the third quarter of 2023 when there were 192,000 jobs lost in the United States. That would stretch that into the fourth quarter and give us kind of a six month stretch of job losses upon revising the Bureau of Labor Statistics survey data with the hard data that we get from the Census Bureau where companies are legally obligated once a quarter to report their headcount. And that’s kind of the ultimate decision, that’s when the ink dries, if you will, on the payrolls data that we see the Bureau of Labor Statistics release.

Simone Del Rosario:

So we’re looking at a recession that would have started in October of last year?

Danielle DiMartino Booth:

I personally see the recession as having started in October 2023 because that’s the first time that the McKelvey rule, which is less arduous than the Sahm rule, and it doesn’t date back to 1948, it dates back to 1968, but it has not missed a single recession since then. Rather than a half a percentage point increase in the unemployment rate off of its lowest level in the prior 12 months, it is a .3 percentage point increase in the unemployment rate again over the prior 12-month period’s low. Again, it has a spotless track record since 1968. It was triggered in October of 2023. The Bureau of Labor Statistics said that we lost 192,000 jobs in the three months ending September the 30th, 2023. So the National Bureau of Economic Research could theoretically backdate it further, but again, the McKelvey rule is what I’ve relied on. The former chief economist at Goldman Sachs, he was interviewed by the Wall Street Journal in January of 2008, when his rule was triggered and he was asked the same question, well, your McKelvey rule was triggered in December of 2007. Do you think we’re in recession? And he said, well, you know, my rule might be broken, basically. But of course, the NBER did backdate that recession to December of 2007, and the McKelvey rule was not broken. Luckily, Bloomberg Economics team agrees with me that recession, that job losses started in October of 2023.

Simone Del Rosario:

Danielle, you’re so good at looking at these types of economic data points and looking beyond the normal monthly releases that we see. Why isn’t the Fed?

Danielle DiMartino Booth:

think the Fed is choosing to look the other way in this instance. There are some regulations that the Fed has been working on that could really define Chair Powell’s legacy that would begin to regulate the private equities, the hedge funds, the BlackRocks of the world, that are in some cases larger than banks if you consider the trillions of dollars that they have under management. And in order to push through with some of these regulations, he really does need hire for longer on his side. He needs hire for longer policy enough to go with what the Bureau of Labor Statistics first reports, even though we know that since January of 2023, we’ve seen one downward revision after another to the data. It’s become systematic. In fact, the persistence with which we’ve seen downward revisions to what’s first reported. But again, I think Powell’s got his own reasons.

Simone Del Rosario:

How do you square this idea that we could be in a recession right now with the GDP numbers that we’re seeing? The latest reading, the advance estimate, showed an annual growth rate of 2.8%.

Danielle DiMartino Booth:

So we had 2-point-something percent in 2001 when it was first reported. Of course, was another six quarters later that we revised it and found out that it was a negative number. It takes magnitudes of the amount of time to get correct unemployment data, correct payrolls data. You can double the time that it takes to figure out what the actual GDP is that’s associated with that time frame. If you find out that you’re 830,000 jobs shy of what you thought you were, which is what we found out in the third quarter of 2023, looking backwards with hard data in hand, then you have to subsequently go back and back out. Well, 830,000 people were not actually working. 830,000 people were not actually producing economic output that we thought were. So you’ve got to back that out. And it takes a lot of time for the Bureau of Labor Statistics data to work its way into subsequent revisions for the Bureau of Economic Analysis data, for GDP. It’s at inflection points. It’s when contractions become expansions, when expansions become contractions, that these big statistical agencies have trouble seeing the turning point given their modeling. But it wasn’t until 2018 that we saw the final GDP revision from the great recession that ended in June of 2009. Again, the recession ended June of 2009. We didn’t get the final revision for GDP for that recession until 2018.

Simone Del Rosario:

Wow. On one hand, this can seem incredibly frustrating if people feel like we’re in a recession, they feel like the economy’s not good, we continue to get, on the surface, economic releases that show a pretty strong economy, but people know what they feel, they know what they’re experiencing and they feel something different. But that said, if, to your point, we are already in a recession, does that take some of the panic away, that we’ve been going through it, or is it going to get worse? What’s your read on that?

Danielle DiMartino Booth:

Well your average recession is 10 months long in the post-war era. So using that average length of time, we should theoretically be starting to recover and coming out of recession. That being said, the Federal Reserve has waited, now 12 months, now longer than 12 months, and the longer it waits, typically the deeper and longer the recession is as a result. There have been some great studies that empirically demonstrate this. The period leading up to the Great Recession, 2007-2009, the Fed waited 15 months. It’s the longest the Fed’s ever waited. So we’re just at the 12-month mark now. But it certainly looks like we’re going to get to the 14-month mark if it’s September the 18th that we can anticipate that first rate cut. So that’s about as long as the Fed has ever waited to provide relief in the form of the beginning of an easing cycle.

Straight to your inbox.

By entering your email, you agree to the Terms & Conditions and acknowledge the Privacy Policy.

MOST POPULAR

-

Getty Images

Getty Images

Democrats in Congress receive lowest approval rating in Quinnipiac poll history

-

Getty Images

Getty Images

AG Bondi reviewing Epstein documents for release, could hold client list

-

Getty Images

Getty Images

Speaker Johnson won’t support DOGE stimulus checks

-

Reuters

Reuters

UN chief reveals his plan for peace in Haiti to Caribbean leaders