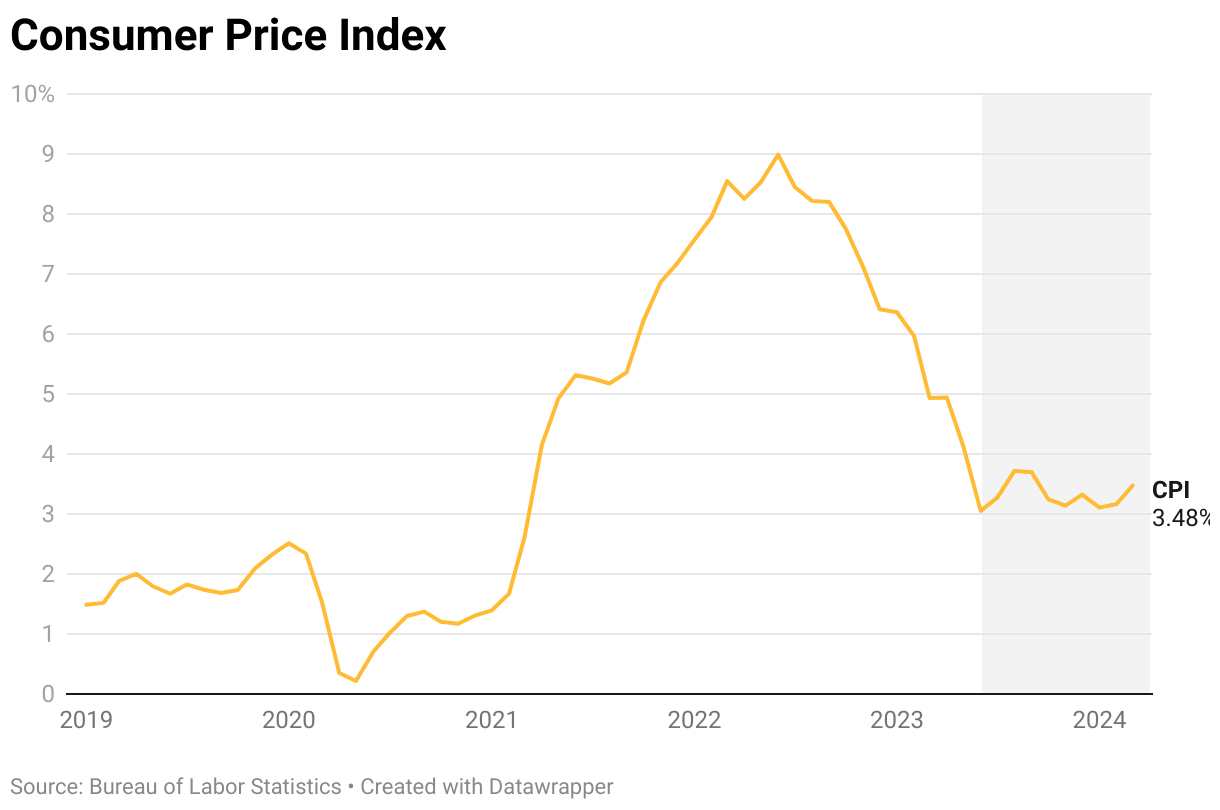

March’s sticky inflation report has thrown into question the timing of the Federal Reserve’s anticipated interest rate cuts. In fact, some have said Americans can’t rule out the Fed going in the opposite direction and hiking the rate instead.

Download the SAN app today to stay up-to-date with Unbiased. Straight Facts™.

Point phone camera here

The Federal Reserve penciled in three quarter-percentage point rate cuts in 2024, but that was before March’s report released during the week of April 7.

Consumer price inflation in March heated up to 3.5% from February’s 3.2% annual rate. While the Fed’s restrictive monetary policy has helped bring inflation down from its 9% peak in June 2022, inflation has been stuck between 3% to 4% for 10 straight months when the target rate is 2%.

The Fed has held the target range between 5.25% and 5.5% since July 2023. The rate reflects what banks charge each other in overnight lending but ripples to other types of consumer borrowing.

“I think we’re seeing in real time what it feels like to have an entire youth in a zero-interest rate environment and then have to adapt to having very high levels of debt in a high-interest rate environment,” Danielle DiMartino Booth, CEO of QI Research and former Federal Reserve adviser, said. “It’s not looking very pretty right now.”

The Philadelphia Fed said credit card delinquencies are the highest on record going back to 2012. U.S. credit card debt is at an all-time high and nearing the 2008 inflation-adjusted record. Meanwhile, the average 30-year fixed mortgage rate is around 7%.

While the number and timing of rate cuts is now in doubt, DiMartino Booth warns that current policy is already very restrictive and could tip into “policy error” territory.

“I think the mistake is not more so that we repeat a second wave of inflation, but rather an overly tight monetary policy exacerbates a weakening job market as well as household finances, which we’re seeing manifest in rising delinquency rates,” she said.

According to DiMartino Booth and QI Research data, non-discretionary inflation — spending necessities — is running at 4.7% year over year, while discretionary inflation — what people want to buy, not what they need — is running at just 0.7%.

“Households really don’t have a lot left over when they cover the costs of essentials, which are crippling, but not in the Fed’s control,” DiMartino Booth said. “We’re talking about gasoline prices, food prices, car insurance, homeowners insurance; these are things over which Federal Reserve policy has absolutely zero, zero, zero influence.”

Watch the interview above for DiMartino Booth’s take on when the Fed will cut rates and if this year’s election plays a role.

Tags: Credit card, Economy, Federal Reserve, Inflation, Interest rates, Philadelphia Federal Reserve Bank

Simone Del Rosario: This is what I picture when I think about the state of inflation right now. Pause that. It’s probably because of headlines like this, media keeps talking about this sticky inflation. Here’s what that looks like.

After peaking at 9% annual inflation and the Federal Reserve hiking interest rates to restrict the money supply to try to bring that inflation down, it did go down. But now we’ve been stuck in this 3% range for 10 months – remember, the target is 2%. And from February to March, it actually went up from 3.2 to 3.5%.

So remember those interest rate cuts that were supposed to happen this year that would make buying a home or borrowing money more reasonable? Now the timing and number of cuts could be in jeopardy.

If this latest hot inflation report says anything, it’s that inflation going down is not a foregone conclusion. Here I lined up the infamous inflation episode of the 1970s with what’s happened this cycle. The paths look very similar. But then look at what happened next. Inflation climbed back up over the next four years to 14%, and it took another three years after that to get down into the 2s.

I want to bring in former Federal Reserve advisor and CEO of QI Research, Danielle DiMartino Booth. Danielle, given what we’re seeing with inflation this year, what do you think the Fed needs to do to make sure that we don’t repeat history like we just saw on that chart?

Danielle DiMartino Booth: Well, I think the Fed would have to work really hard to have an influence on on the future as opposed to trying to, to not repeat history. Unfortunately, when you when we were going into that second wave of supply chaat supply shock driven inflation, we were also creating quite a few jobs. And the opposite dynamic holds today. And I think that the Fed is in the process, potentially, of making a policy error and not recognizing that, specifically, we’re, you know, not even midway through April, and we’ve had more than 300,000 job cuts announced this year, true inflation Tru which bond traders put on my radar screens running at 1.74%. And depending on whether or not you’re talking about food being the shortest housing being the longest, there’s a one to nine month lead time between translation and headline CPI. To get a little in the weeds here. There’s a point nine seven correlation between true inflation and headline CPI meaning real time data metrics are telling us that, that what’s ahead for the Fed is that inflation is actually going to be running below its target at a time of increasing joblessness and other words, is probably overly tight with its policy in present times. So I think the mistake is not more so that we repeat a second wave of inflation but rather than overly tight monetary policy exacerbates a weakening job market as well as household finances which we’re seeing manifest in rising delinquency rates.

Simone Del Rosario: So you’re not concerned with the fact that inflation has stayed in this three to 4% range for 10 months now, what you’re looking at actually predicts that this is going to dive down that we are on the right path, at least as far as inflation is concerned. Well,

Danielle DiMartino Booth: Remember inflation in some ways is also a reflection of pricing power. It is highly problematic. And I’m not insensitive to the fact that when you look at the price pressures for household essentials, non discretionary inflation, which we run it Qi research is a separate series that’s running at 4.7% year over year. And that’s very problematic for households. Inflation for discretionary purchases, these are the things that we want to buy, we want to buy airplane tickets and concert tickets and go stay in hotels that trying to get oh point 7%, showing you that household really don’t have a lot left over when they cover the costs of essentials, which are crippling, but again, not in the Feds control. We’re talking about gasoline prices, food prices, car insurance, homeowners insurance, these are things ever which Federal Reserve policy has absolutely 000 influence.

Simone Del Rosario: So given all of that, what should we be looking at as far as the rate environment this year? I know a lot of people were really hopeful about these upcoming rate cuts. former Treasury Secretary Larry Summers says Now we can’t rule out a rate hike being the Feds next move. What do you think is the right move?

Danielle DiMartino Booth: So I think it’s a slippery slope to really get too deep into discussion right now about rate hikes. Given that as as far as the law is concerned, today, the Fed retains its dual mandate of minimizing inflation and maximizing employment because of the stresses that we’re seeing emerge, maybe not through your headline initial jobless claims, maybe not through non farm payrolls, but certainly in the increases that we’re seeing in the unemployment rate. Given that, you know, I think that that is where the Feds focus should be not looking at tightening further in this environment. Because certain areas of essentials are again out of the Feds control are rising. I think. I think Summers is a bit premature in making that declaration. Because we’re not very far away from call it 3.85% and 3.95%. Rounding up to 4%, which is the Feds year end unemployment rate target.

Simone Del Rosario: So are you thinking still rate cuts this summer? I’m trying to get a gauge on this. You know, I

Danielle DiMartino Booth: I actually don’t think that this summer is in the cards. But I think that there is something to be said for the possibility of maybe, maybe July. September is a toss up given in any given election year, the FOMC meeting that directly precedes a presidential election is a 5050 chance as to whether the Fed makes a move, whether they’re in a tightening or an easing regime. And then that just leaves you with November in December. So I think it’s difficult to get to the three that were still being projected by Fed officials in the March dotplot. But I certainly do see the possibility of there still being two rate cuts this year.

Simone Del Rosario: I think the Fed would have liked to be making moves earlier in the year given that it is an election year, the closer that we get to the election, how does that throw a wrench into how the Fed moves?

Danielle DiMartino Booth: Well, you may or may not have noticed this is a fairly delicate presidential election year, tensions are running higher than they would normally. And that means that that the Fed is going to be under more scrutiny than it would be in any other presidential election year to not be viewed as trying to sway the outcome of the election one way or the other. Because Jay Powell, is one of the least political Fed Chair since Paul Volcker was in office, I would say that the risk is that they lean to the to the side of, of easing less than they would otherwise in 2024. The magnitude that they’re discussing cutting rates by if you’re really talking about a quarter of a percentage point, it’s not going to do anything, it’s not going to do anything for the economy, when we’re still contending with the lag effects of the tightening campaign that have yet to work their way through the economy. But we live in a world it’s driven by social media and perceptions, and there will be accusations. Either way, regardless of what the Fed does or does not do. I don’t think we can get past that. Again, given how divisive right now, the electorate is.

Simone Del Rosario: You talked about how these these quarter point cuts that could potentially be down the line. I mean, they’re so minuscule and what we’re looking at, I’m a millennial, in my adult life, we have not seen long term high interest environment, I wanted to ask you what that would look like I think we’re so used to for in recent history rates being pretty low that what would it look like if they held rates higher for longer?

Danielle DiMartino Booth: You know, I think we’ve actually already seen that Philadelphia Fed came out with fresh data overnight that showed that the percentage of Americans making the minimum credit card payment is at the lowest on record. And credit card delinquencies. This is a data series back to 2012. It’s fairly young, but that the percentage of Americans who are delinquent on their credit cards is at the highest in the 12 year history of that data series, I think we’re seeing in real time, what it feels like to have an entire youth in a zero interest rate environment and then have to adapt to having very high levels of debt. In a high interest rate environment. It’s not looking very pretty right now.

Simone Del Rosario: And then I wanted to ask you about this on a wider scale, if interest rates continue to stay this high, especially considering how much national debt there is, what impact does that have on the national debt? And is it sustainable? I know this kind of goes outside the realm of what the Federal Reserve controls, but certainly it’s something that the nation is dealing with or that Congress shouldn’t be dealing with.

Danielle DiMartino Booth: You know, well, what’s interesting, of course, is is that with the with the divided Congress, it’s difficult to just keep the lights on. So there hasn’t really been any, any at the margin new spending initiatives, if you will. But of course, you know, we’re going to get across a trillion dollars in interest expense, that’s certainly something that gathers headlines. But on a practical level, the more we spend on interest expense, which you could think of as an effective sunk cost, the less we’re going to be able to legislate if and when, depending on the construct of Congress, after Election Day in the new Congress is sworn in, the more we’re spending on interest, the less we’re going to be able to legislate, to provide some relief for the recession that I believe we will certainly be in by then. if not sooner, so. But again, at the margin, we’re really not spending as much as what the mainstream media would have you believe. And when I say at the margin, I mean, I mean, in addition to money that’s already been legislated. Right,

Simone Del Rosario: Danielle DiMartino Booth, CEO of QI Research, we’ll leave it there. Thank you so much for your insights always.

Danielle DiMartino Booth: Thank you very much. Take care.

MOST POPULAR

-

AP Images

AP Images

N. Korea hackers steal military secrets, hit Air Force bases, NASA, US says

-

Getty Images

Getty Images

A convicted child rapist is competing in Paris Games, many want to know why

-

AP

AP

Barack and Michelle Obama endorse Kamala Harris for president

-

Reuters

Reuters

Attacks disrupt trains ahead of Olympics opening ceremony