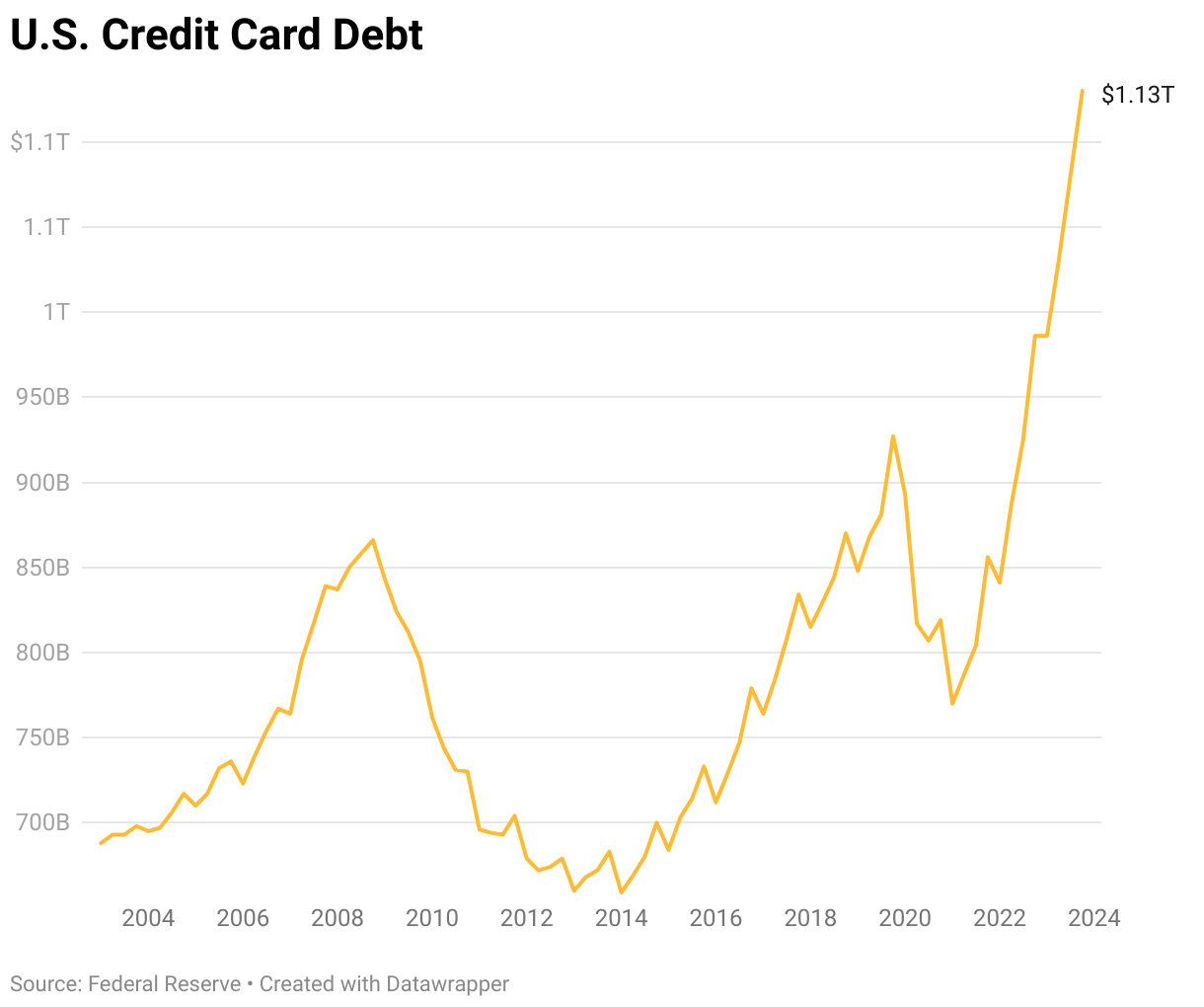

Credit card debt in the U.S. hit a record at the end of 2023 while high interest rates continue to push the debt balance even higher this year. The Federal Reserve recently reported U.S. credit card debt reached $1.13 trillion in the fourth quarter of 2023, up $143 billion from the year before. According to WalletHub, the total already topped $1.3 trillion by January.

“Context is important,” Bankrate Chief Financial Analyst Greg McBride said. “We’re at a higher level of population than we’ve ever been before. We’ve also seen tremendous inflation.”

Download the SAN app today to stay up-to-date with Unbiased. Straight Facts™.

Point phone camera here

When adjusted for inflation, WalletHub calculates total credit card debt is about 10% off its peak, which the country hit in 2008 during the Great Recession. But the CEO said growing balances this year could put the inflation-adjusted record in striking distance.

“We’ve had more people carrying larger balances for a longer period of time, at a time when credit card rates are at a record high,” McBride said. “And oh, by the way, delinquencies are the highest since 2012. So you put that all together, there’s no explaining that away that everything’s fine. Sixty percent of households are living paycheck to paycheck and clearly there everything is not fine.“

There’s typically a lot of shame around credit card debt, but credit card experts say that shame is often misguided.

“There’s definitely this idea that credit card debt is always the result of frivolous spending — you’re shopping, you’re going out, you’re buying stuff you shouldn’t buy that you don’t need,” NerdWallet credit cards expert Sara Rathner said. “The reality for a lot of people is credit cards are what are helping them make it from week to week.”

Higher prices, more debt

A NerdWallet survey revealed that 48% of Americans with revolving credit card debt are charging necessities, like food.

“What’s made this bout of inflation so insidious is that it’s hit hardest on necessities,” McBride said. “Shelter, food, energy costs — even things like automobile insurance.”

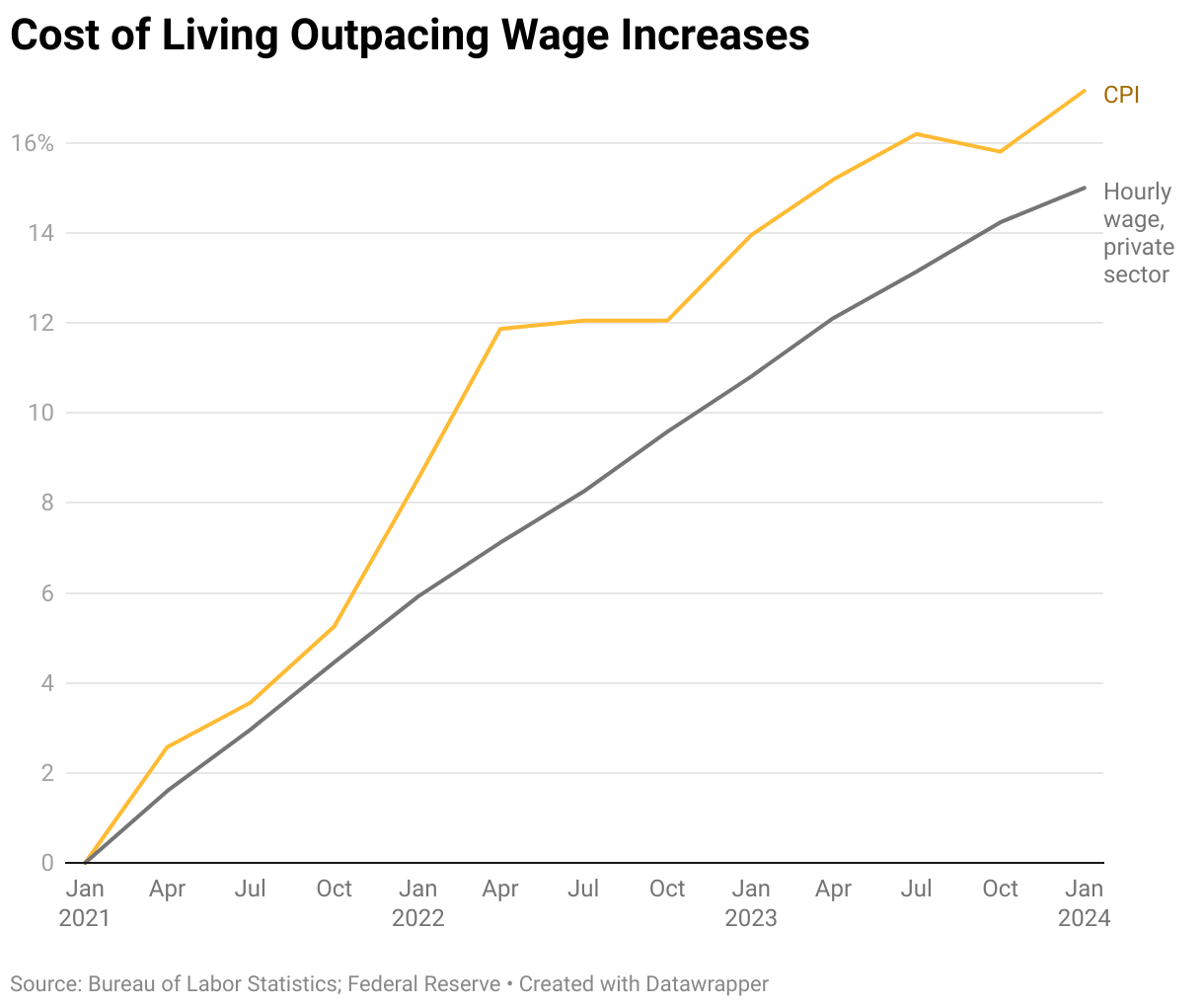

Since January 2021, the cost of living has been rising faster than the private sector’s average hourly wage, according to data by the Bureau of Labor Statistics and the Federal Reserve. At the same time, Americans’ personal savings are draining after COVID-19 peaks.

“If you don’t have much of a cushion of savings, you have no buffer between you and credit card debt the next time an unplanned expense arises,” McBride said.

For the second consecutive year, more than a third of Americans say they have more credit card debt than emergency savings. At 36%, Bankrate said it’s the highest percentage since they started asking this question in 2011. Gen Xers and millennials are driving the trend, which McBride said is not surprising.

“Those are the prime years of rising household expenses,” he said. “You’re buying houses, buying cars, raising a family, putting kids through college.”

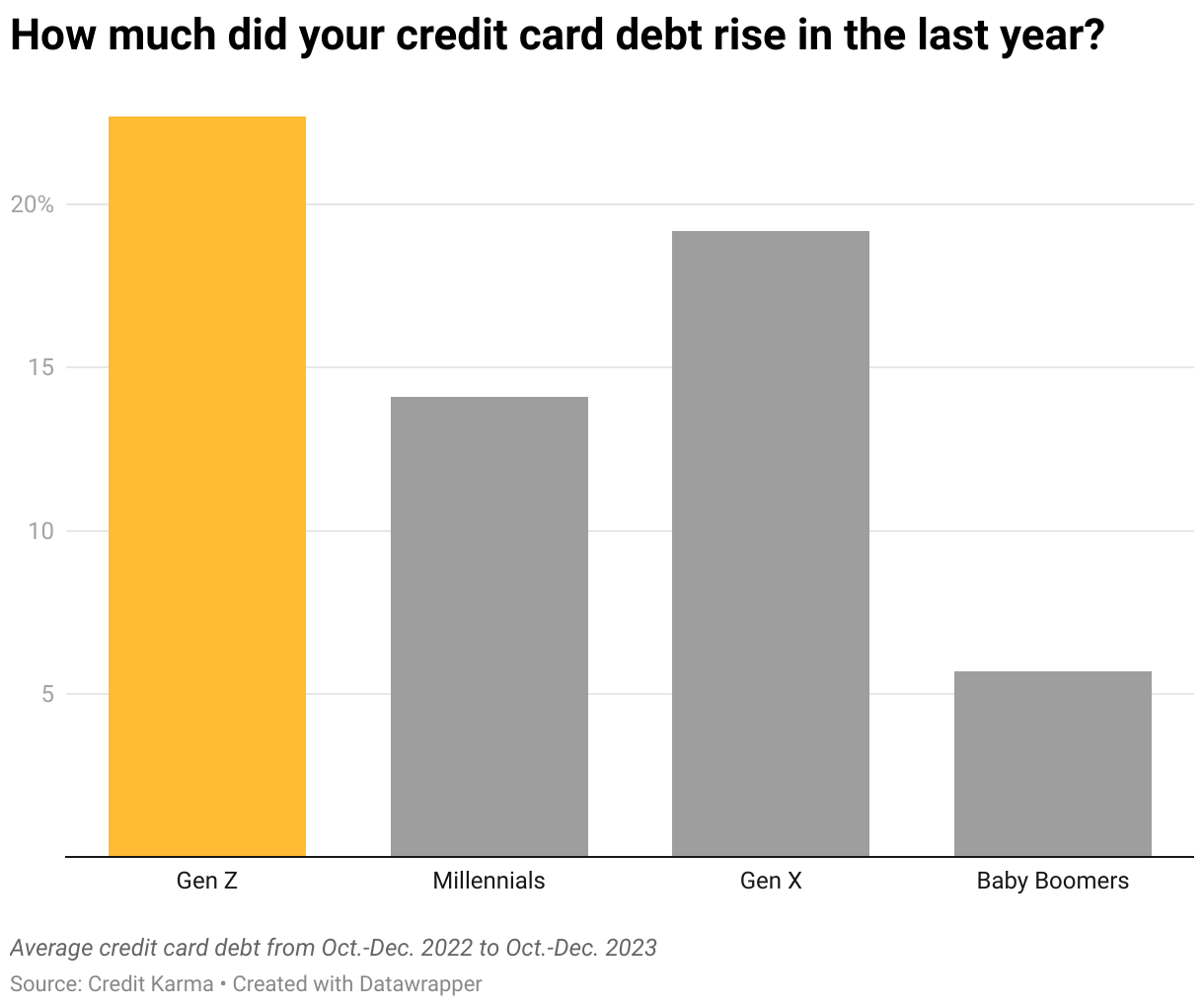

Gen Z’s credit card debt is growing faster than any other generation. Credit Karma said the average debt balance went up nearly 23% from 2022 to 2023.

“I really feel for the younger generation now that’s just beginning to enter the workforce because it is very hard out there,” Rathner said. “Costs are up, wages are not up as much as costs and interest rates are really high.”

Higher interest rates, more debt

Bankrate reports that 49% of surveyed credit card users carry a balance month to month, up from 39% in 2021. In today’s interest rate environment, getting out from under that debt can seem insurmountable.

“It just becomes another bill that you pay every month,” Rathner said. “That’s really what it looks like for people who are in never-ending credit card debt.”

Take the current average credit card debt of $6,360, according to TransUnion. Without taking on any additional debt, if this person only makes minimum payments of around $174.90 a month, paying the average interest rate of around 21%, they’ll spend more than 25 years paying off the card. And they’ll pay more than $10,000 in interest alone. These calculations come from Bankrate’s minimum payment calculator.

Paying down debt

For those facing crippling credit card debt, experts say a great option to chip away at it is moving that debt to a balance transfer card with a zero-or-low-interest introductory rate. The problem is these cards are hard to come by if the person doesn’t have good or excellent credit.

“Look at contacting a nonprofit credit counseling agency who could really help you with things like budgeting, debt management, those types of things, get you pointed in the right direction,” McBride said.

“It might even mean declaring bankruptcy at some point if you really don’t see a way out of your debt,” Rathner said.

NerdWallet said about a third of Americans who carry a balance month to month believe they’ll be in credit card debt forever.

“Once you get into credit card debt, it is hard to get out,” Rathner said.

Tags: Bankrate, Bureau of Labor Statistics, Consumer Price Index, Credit card, Credit Karma, Federal Reserve, Inflation, Interest rates, Minimum wage, NerdWallet, U.S. Economy, Wages, WalletHub

Family Guy Clip: I have $30,000 in credit card debt.

Simone Del Rosario: Peter Griffin, you’ve got company.

Social media clip: I ended up racking up $25,000.

Social media clip: I’m over here drowning.

Social media clip: I think I’m $20,000 in credit card debt.

Social media clip: The balance right now is $18,821.53.

Simone Del Rosario: While some people are vulnerable enough to share their debt journeys on social media, there’s typically a lot of shame around credit card debt.

Social media clip: I feel bad enough. Please don’t come in the comments talking about how irrespon- I know. I know.

Simone Del Rosario: And credit card experts say that shame is often misguided.

Sara Rathner: There’s definitely this idea that credit card debt is always the result of frivolous spending, you’re shopping, you’re going out, you’re buying stuff you shouldn’t buy that you don’t need. The reality for a lot of people is credit cards are what are helping them make it from week to week.

Simone Del Rosario: The Federal Reserve reports U.S. credit card debt reached an all-time high at the end of 2023 at $1.13 trillion. That’s up $143 billion from the year before.

Greg McBride: Context is important. We’re at a higher level of population than we’ve ever been before. You know, we’ve also seen tremendous inflation.

Simone Del Rosario: When adjusted for inflation, WalletHub says total credit card debt is about 10% off its peak, which the country hit in 2008 during the Great Recession. But the CEO said growing balances this year could put the inflation-adjusted record in striking distance.

Greg McBride: We’ve had more people carrying larger balances for a longer period of time, at a time when credit card rates are at a record high. And oh, by the way, delinquencies are the highest since 2012. So you put that all together, I mean, there’s there’s no explaining that away that everything’s fine. Sixty percent of households are living paycheck to paycheck and clearly there everything is not fine.

Simone Del Rosario: A NerdWallet survey reveals about half of Americans with revolving credit card debt are charging necessities, like food.

Greg McBride: What’s made this bout of inflation so insidious is that it’s hit hardest on necessities, shelter, food, energy costs, even things like automobile insurance.

Simone Del Rosario: Since January 2021, the cost of living has been rising faster than the private sector’s average hourly wage. At the same time, Americans’ personal savings are draining after COVID-19 peaks.

Greg McBride: If you don’t have much of a cushion of savings, you have no buffer between you and credit card debt the next time an unplanned expense arises.

Simone Del Rosario: For the second consecutive year, more than a third of Americans say they have more credit card debt than emergency savings. It’s the highest percentage since Bankrate started asking this question in 2011. Gen Xers and millennials are driving the trend, which Bankrate’s Greg McBride says makes sense.

Greg McBride: Those are the prime years of rising household expenses, you’re buying houses, buying cars, raising a family, putting kids through college.

Simone Del Rosario: But Gen Z’s credit card debt is growing faster than any other generation. Credit Karma says it went up nearly 23% in one year.

Sara Rathner: I really feel for the younger generation now that’s just beginning to enter the workforce because it is very hard out there. Costs are up, wages are not up as much as costs. And interest rates are really high.

Social media clip: You guys, the interest is what kills me. I get charged like $400 in interest a week.

Simone Del Rosario: Bankrate says about half of credit card users carry a balance month to month, up from 39% in 2021. And in today’s interest rate environment, getting out from under that debt can seem insurmountable.

Tooth Fairy movie clip: It’s like credit card debt, man. They just want to keep you paying forever.

Sara Rathner: It just becomes another bill that you pay every month. That’s really what it looks like for people who are in never ending credit card debt.

Family Guy clip: Credit card debt, credit card debt, credit card debt.

Simone Del Rosario: Take the average credit card debt of $6,360. Without taking on any additional debt, if this person only makes minimum payments with the average interest rate of around 21%, they’ll spend more than 25 years paying off the card. And they’ll pay more than $10,000 in interest.

Family Guy clip: I don’t have as cavalier an attitude toward my debt as the song suggests. I’m actually up most nights with severe panic attacks.

Simone Del Rosario: For those facing crippling credit card debt, experts say a great option to really chip away at it is moving that debt to a balance transfer card with a zero-or-low-interest introductory rate. The problem is these cards are hard to come by if you don’t have good or excellent credit.

Greg McBride: Look at contacting a nonprofit credit counseling agency who could really kind of help you with things like budgeting, debt management, those type of things kind of get you pointed in the right direction.

Sara Rathner: It might even mean declaring bankruptcy at some point, if you really don’t see a way out of your debt.

Simone Del Rosario: NerdWallet says about a third of Americans that carry a balance month to month believe they’ll be in credit card debt forever.

Sara Rathner: Once you get into credit card debt, it is hard to get out.

Simone Del Rosario: Hard, but not hopeless.

Social media clip: I just paid off $31,597 worth of credit card debt.

Social media clip: I paid off $12,400 in credit card debt.

Social media clip: I just paid off two credit cards, baby.

MOST POPULAR

-

AP Images

AP Images

N. Korea hackers steal military secrets, hit Air Force bases, NASA, US says

-

Getty Images

Getty Images

A convicted child rapist is competing in Paris Games, many want to know why

-

AP

AP

Barack and Michelle Obama endorse Kamala Harris for president

-

Reuters

Reuters

Attacks disrupt trains ahead of Olympics opening ceremony