Americans are facing a record amount of credit card debt in 2024 at more than $1 trillion total. Adjusted for inflation, WalletHub says credit card debt is about 10% below its peak, which Americans hit in 2008 during the Great Recession. However, WalletHub estimates growing balances this year could put the inflation-adjusted record in striking distance.

While Americans set the inflation-adjusted record during a dire economic time for the country, higher debt levels do not always spell trouble. In fact, rising debt can boost economic growth, at least for a while.

When higher household debt is a boon

Economists measure the health of a country’s economy by calculating its gross domestic product, which is essentially adding up all of the economic activity in the country. The single most influential part of that equation is consumer spending. It makes up about two-thirds of U.S. GDP.

And though consumers are starting to charge more purchases – credit card debt went up more than 14% in the past year – spending has yet to take a major hit. Economists point to the strong labor market as one reason why.

If the job market takes a turn, Americans may start to rein in that spending. But for now, they seem willing to take on more debt.

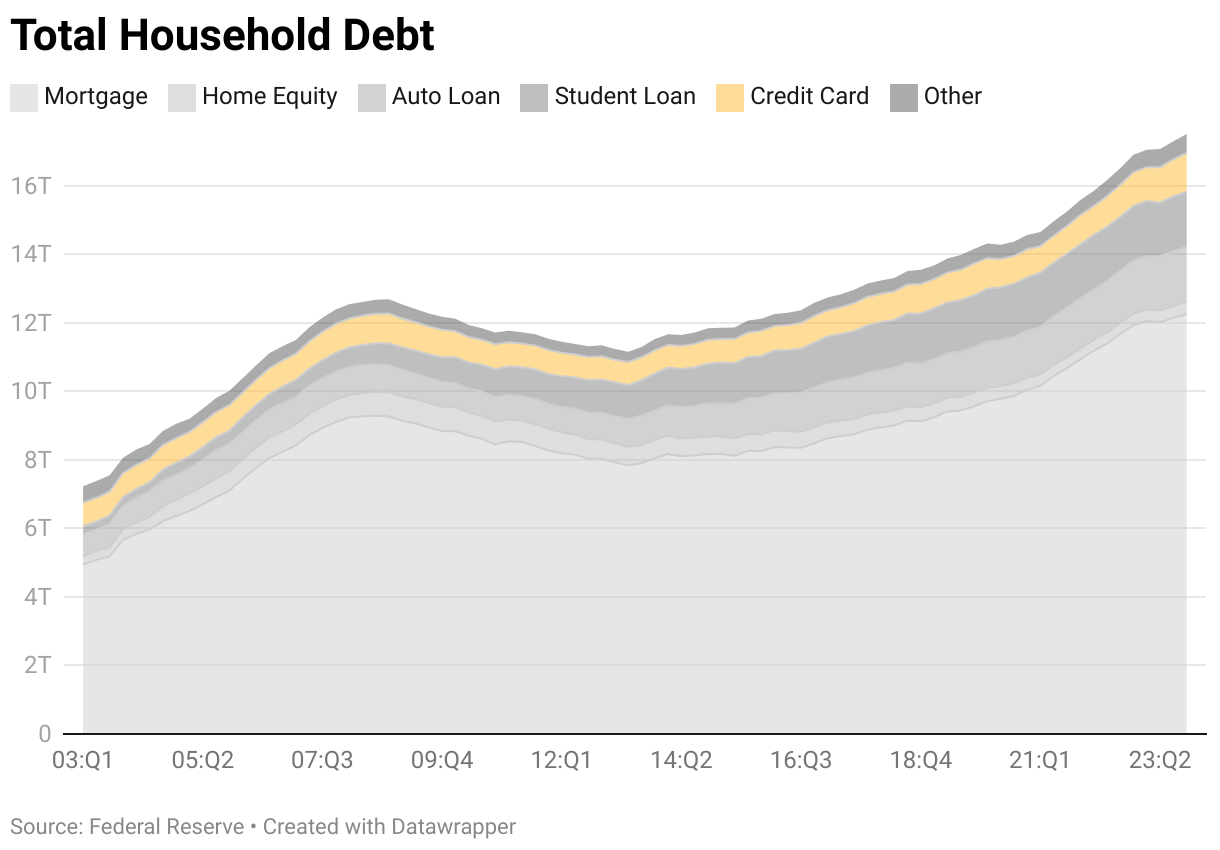

In fact, the Federal Reserve reported household debt is at a record high of $17.5 trillion. Most of that is made up of mortgages but also includes auto loans, student loans, and credit card debt. Credit cards, far and away, experienced the biggest percentage increase year over year.

A study by the Bank for International Settlements analyzing dozens of economies found that rising household debt boosts a country’s GDP growth, at least in the short term. In the longer run, they found that a 1 percentage point increase in the household debt-to-GDP ratio tends to lower growth by 0.1 percentage point.

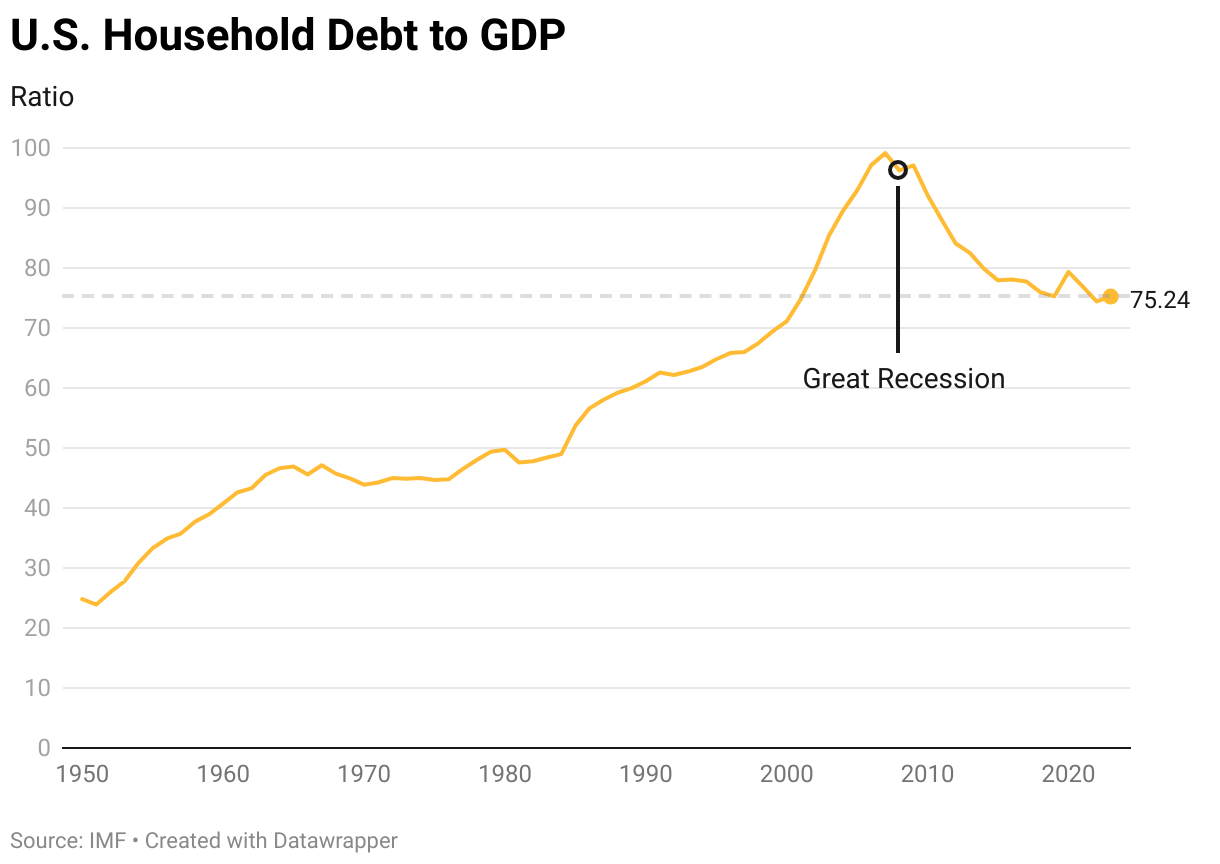

Household debt low when compared to GDP

Household debt as a percentage of GDP is pretty close to the bottom of levels the country has experienced since 2001.

“Debt level growth in recent months appears to be in line with wage growth, so at this point, it doesn’t seem to be raising a red flag,” said Rob Haworth, senior investment strategy director at U.S. Bank Wealth Management. “If people are borrowing more money, the question is whether they are in a position to pay it back.”

Can Americans afford debt payments?

Economists measure whether society as a whole can afford debt payments by calculating those service payments as a percent of disposable income, which is income after taxes. The only time in recent history this has been lower than now was during the COVID-19 pandemic when people got stimulus checks and didn’t have many places to go to spend money.

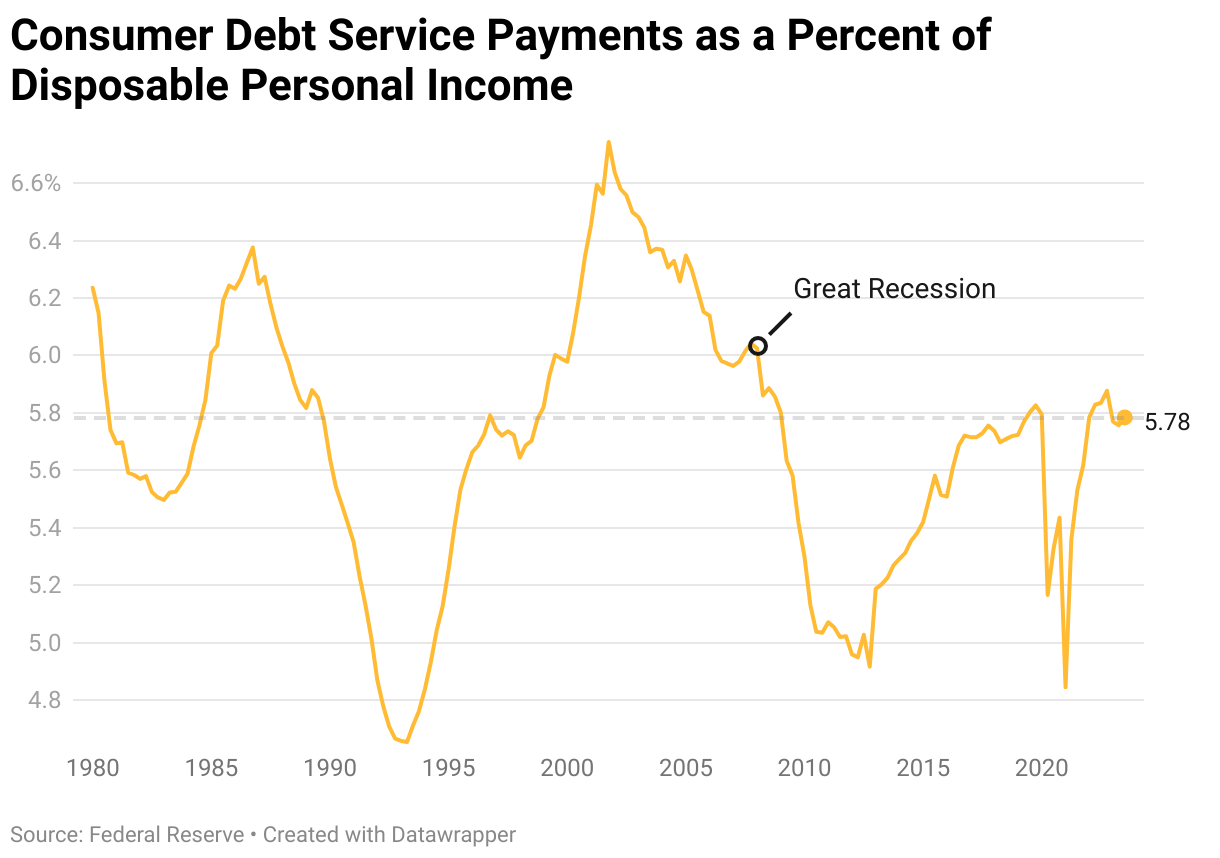

If you strip out mortgage debt from this equation, the percentage is sitting a bit higher historically, but it’s still well below the levels that spelled trouble ahead of the Great Recession.

This doesn’t mean individuals are not struggling with credit card debt. Half of credit card users are carrying a balance month to month, and a third of those believe they’ll be in credit card debt forever. We dig into why more people are charging purchases today and what they’re buying here.

Tags: Bank for International Settlements, COVID-19, Credit card, credit card debt, Economy, Federal Reserve, GDP, Great Recession, Household debt, Inflation, Jobs, NerdWallet, Recession, U.S. Bank, U.S. Economy, WalletHub

Simone Del Rosario: Is rising credit card debt a good thing for the economy? Let’s look into this.

Not adjusted for inflation, U.S. credit card debt right now is at an all-time high. It’s well over a trillion dollars.

Adjusted for inflation, WalletHub says it’s about 10% below peak credit card debt in 2008. You know, when the recession was so bad they gave it a proper name.

On a personal level, the Dave Ramseys of the world will tell you that all debt is bad debt.

Dave Ramsey: When you have debt, you are susceptible to getting your freaking head taken off.

Simone Del Rosario: But when it comes to the greater economy, higher household debt can be a boon.

Mean Girls clip: The limit does not exist.

Simone Del Rosario: Ok, the limit doesn’t not exist. There is a limit. Let’s just dig in.

We measure the health of a country’s economy by calculating its gross domestic product, which is essentially adding up all of the economic activity in the country.

The single most influential part of that equation is consumer spending. It makes up about two-thirds of U.S. GDP.

And though consumers are starting to charge more purchases – credit card debt went up more than 14% in the past year – spending has yet to take a major hit.

Economists point to the strong labor market as one reason why.

If the job market takes a turn, Americans may start to rein in that spending. But for now, they seem willing to take on more debt.

In fact, the Federal Reserve reports household debt is at a record high of $17.5 trillion. Most of that’s mortgages but also includes auto, student, and credit card debt. And credit cards, far and away, experienced the biggest percentage increase.

A study by the Bank of International Settlements analyzing dozens of economies found that rising household debt boosts a country’s GDP growth, at least in the short term. In the longer run, they found that a 1 percentage point increase in the household debt-to-GDP ratio tends to lower growth by 0.1 percentage point.

So how is the U.S. sitting?

Household debt as a percentage of GDP is pretty close to the bottom of levels we’ve seen since 2001. In fact, looking at this chart, you can see the danger levels where households really overleveraged ahead of the Great Recession. We don’t currently see that trend today.

According to Rob Haworth, senior investment strategy director at U.S. Bank Wealth Management, “Debt level growth in recent months appears to be in line with wage growth, so at this point, it doesn’t seem to be raising a red flag.”

He added, “If people are borrowing more money, the question is whether they are in a position to pay it back.”

So let’s take a look at that.

This is looking good: Household debt payments as a percent of disposable income, that’s income after taxes. The only time in recent history this has been lower than now was during the pandemic when people got stimulus checks and there really wasn’t anywhere to spend money.

Now strip out mortgage debt, and this percentage is sitting a bit higher historically. But it’s still well below the levels we saw that spelled trouble ahead of the Great Recession.

This doesn’t mean individuals are not struggling with credit card debt. Half of credit card users are carrying a balance month to month, and a third of those believe they’ll be in credit card debt forever. We dig into why more people are charging purchases today and what they’re buying in this story on SAN.com.

MOST POPULAR

-

AP Images

AP Images

N. Korea hackers steal military secrets, hit Air Force bases, NASA, US says

-

Getty Images

Getty Images

A convicted child rapist is competing in Paris Games, many want to know why

-

Reuters

Reuters

Attacks disrupt trains ahead of Olympics opening ceremony

-

Getty Images

Getty Images

Philly workers furious over mayor’s order that they return to their offices