It was meant to be the insurance of last resort. But along the way, Florida’s government-backed Citizens Property Insurance Corporation became the largest insurance provider in the state.

“Citizens Property Insurance, which was created decades ago, it is not solvent, and we can’t have millions of people on that, because if a storm hits, it’s going to cause problems for the state,” Florida Gov. Ron DeSantis said in February 2024.

Point phone camera here

Then came two storms back to back. Together, Hurricanes Helene and Milton caused tens of billions of dollars in insured losses. Is Citizens up to the task?

“They are actually very financially secure this year,” Proffesor Charles “Chuck” Nyce, who serves as department chair of Florida State University’s Risk Management and Insurance, said. “I believe what Gov. DeSantis was trying to say is that we don’t want Citizens having this type of exposure and having the need to do assessments.”

Assessments happen when Citizens does not have enough money to pay its claims. First, it applies a surcharge to its own policyholders. But if that is not enough, the state requires Citizens to charge a premium to insurance holders statewide, whether with Citizens or not. Citizens will have to do this for as many years as it takes to plug the deficit.

They were designed to be the market of last resort…For 2021, 2022, 2023, Citizens was becoming the option of first resort.

Chuck Nyce, expert in risk management and insurance

Citizens told Straight Arrow News it “has the financial capability to handle a 1-in-82-year storm without having to levy assessments on non-Citizens policyholders.” For context, Citizens says 1992’s Hurricane Andrew was a 1-in-43-year event.

“Hurricane Andrew is what we kind of describe as a wake-up call,” Nyce said. “It was really the first experience for the insurance industry of what a large-scale catastrophe could look like in the United States. I started graduate school the year after Hurricane Andrew. So my entire academic career has been trying to figure out how to pay for catastrophes that can occur.”

Hurricane Andrew bankrupted several insurance companies, leaving hundreds of thousands in Florida without insurance. Other major insurance providers dramatically mitigated their risk in the state by shifting their focus more inland.

“Now the problem is, for the state of Florida, we have a lot of coastal exposure, so we had to find a way to still insure those properties that were out there,” Nyce said.

If we can solve it in Florida, it’ll be a great lesson to take to other states.

Chuck Nyce, expert in risk management and insurance

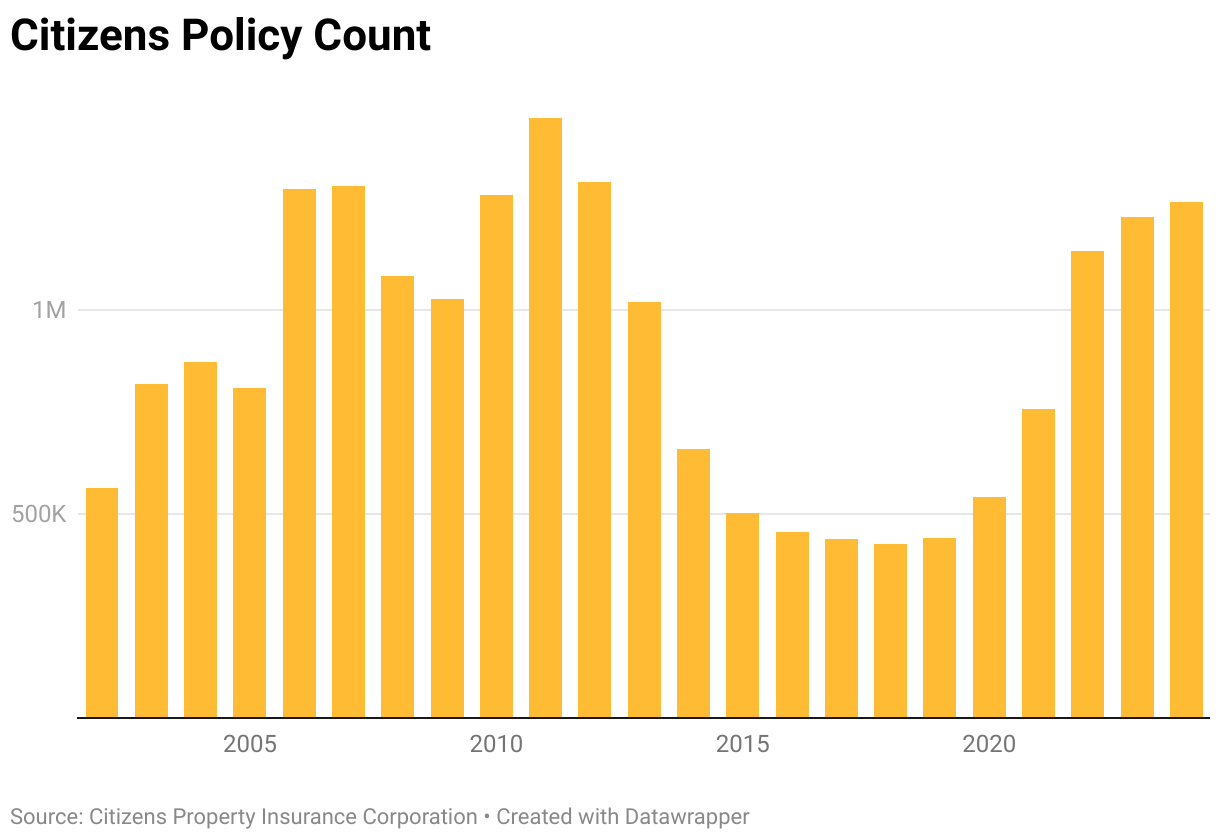

Local companies popped up to fill the gaps, while the state created two insurers of last resort that later merged in 2002 to become Citizens Property Insurance Corporation. Nyce said the system worked well until 2004 and 2005, when storms repeatedly hit the Sunshine State, causing tens of billions in losses.

For Florida’s insurance landscape, it was Groundhog Day. Insurance companies dried up and more left the state. But this time, they had a backstop in Citizens, and Citizens’ policies ballooned.

“They were designed to be the market of last resort,” Nyce said. “By 2010, 2011, there were 1.4 million policyholders in Citizens. The good news for the state is from 2005 through 2016 we didn’t have any landfalling storms.”

Citizens successfully shed policies back into the private market until it was down to a little more than 400,000 by 2019. But more storms and litigation costs again broke the private market.

“For 2021, 2022, 2023, Citizens was becoming the option of first resort,” Nyce said. “There was a number of areas where insurance was not available and not available at a fair price. So Citizens became the option.”

Policies swelled back to over 1 million in 2022 and now sit at 1.265 million as of Oct. 4, 2024.

In order to get customers off the state-backed Citizens and back into the private market, a private insurance provider must be willing to underwrite the client at a price that is no more than 20% higher than what they pay at Citizens. At that point, Citizens can “depopulate” that customer.

Depopulation is “trying to push Citizens back to a market of last resort rather than a first choice,” Nyce explained.

“I think it’s more attractive today to offer policies than it was over the last 20 years,” DeSantis said in February. “But, you know, Rome wasn’t built in a day.”

Get up to speed on the stories leading the day every weekday morning. Sign up for the newsletter today!

By entering your email, you agree to the Terms & Conditions and acknowledge the Privacy Policy.

Citizens told SAN that before Hurricanes Helene and Milton, it expected to dip below 1 million policies by the end of 2024. These storms could put that goal in jeopardy.

“When losses get really bad, that’s when the state should come in,” Nyce said. “When they get really, really bad, that’s when the federal government should come in. But for the storms like Helene, that should be private market stuff that’s handling those types of things. But it’s an issue we have.”

Nyce said from an insurance perspective, homeowner policies used to be considered low-risk and relatively stable. But that’s no longer the case in much of the United States, andnd that’s when states see the private market disintegrate.

“If we can solve it in Florida, it’ll be a great lesson to take to other states,” Nyce said.

When it comes to insurance risks, it’s not just hurricanes in Florida and Louisiana. It’s wildfires in California, tornadoes in the Midwest and severe convective storms hitting everywhere in between. Florida may be the tip of the spear for storm exposure, but it does not stand alone.

Tags: Bankruptcy, Florida, Florida State University, Home insurance, hurricane, Hurricane Helene, Hurricane Ian, Hurricane Milton, Hurricane season, Insurance, insurance premium, Ron DeSantis, State Farm

Simone Del Rosario: It was meant to be the insurance of last resort. But along the way, Florida’s government-backed Citizens Property Insurance Corporation became the largest insurance provider in the state.

Ron DeSantis: Citizen’s property insurance, which was created decades ago, it is not solvent, and we can’t have millions of people on that, because if a storm hits, it’s going to cause problems for the state.

Simone Del Rosario: Then came two storms back to back. Together, Hurricanes Helene and Milton caused tens of billions of dollars in insured losses. Is Citizens up to the task?

Chuck Nyce: They are actually very financially secure this year. I believe what Governor DeSantis was trying to say is that, you know, we don’t want Citizens having this type of exposure and having the need to do assessments.

Simone Del Rosario: Assessments happen when Citizens doesn’t have enough money to pay its claims. First, it applies a surcharge to its own policyholders. But if that’s not enough, the state requires Citizens to charge a premium to insurance holders statewide, whether with Citizens or not. And it does this for as many years as it takes to plug the deficit.

Citizens told Straight Arrow News it “has the financial capability to handle a 1-in-82-year storm without having to levy assessments on non-Citizens policyholders.” For context, Citizens says 1992’s Hurricane Andrew was a 1-in-43-year event.

Chuck Nyce: Hurricane Andrew is what we kind of describe as a wake-up call. It was really the first experience for the insurance industry of what a large-scale catastrophe could look like in the United States. My name is Chuck Nyce. I am a full professor at Florida State University. My expertise is catastrophic risk financing. I started graduate school the year after Hurricane Andrew. So my entire academic career has been trying to figure out how to pay for catastrophes that can occur.

Simone Del Rosario: Hurricane Andrew bankrupted several insurance companies, leaving hundreds of thousands without insurance. Other major insurance providers…

Chuck Nyce: I’m not going to mention company names, but these are the companies that advertised during the Super Bowl

Simone Del Rosario: …dramatically mitigated their risk in the state by shifting their focus more inland.

Chuck Nyce: Now the problem is, for the state of Florida, we have a lot of coastal exposure, so we had to find a way to still insure those properties that were out there.

Simone Del Rosario: Local companies popped up to fill the gaps, while the state created two insurers of last resort that later merged in 2002 to become Citizens Property Insurance Corporation.

Chuck Nyce: That worked for a number of years, up until 2004, 2005, when we had, again, a combined, at the time, $35 billion in losses.

Simone Del Rosario: For Florida’s insurance landscape, it was Groundhog Day. Insurance companies dried up, more left the state, but this time, they had a backstop, and Citizens’ policies ballooned.

Chuck Nyce: They were designed to be the market of last resort. By 2010, 2011, there were 1.4 million policyholders in Citizens. The good news for the state is from 2005 through 2016 we didn’t have any landfalling storms.

Simone Del Rosario: Citizens successfully shed policies back into the private market until it was down to around 400,000 by 2019. But more storms and litigation costs again broke the private market.

Chuck Nyce: For 2021, 2022, 2023, Citizens was becoming the option of first resort. There was a number of areas where insurance was not available and not available at a fair price. So Citizens became the option.

Simone Del Rosario: Policies swelled back to over a million and now sit at more than one and a quarter.

In order to get customers off the state-backed Citizens and back into the private market, a private insurance provider must be willing to underwrite the client at a price that is no more than 20% higher than what they pay at Citizens. At that point, Citizens can “depopulate” that customer.

Chuck Nyce: Trying to push citizens back to a market of last resort rather than a first choice.

Ron DeSantis: I think it’s more attractive today to offer policies than it was over the last 20 years. But, you know, Rome wasn’t built in a day.

Simone Del Rosario: Citizens told SAN that before Hurricanes Helene and Milton, it expected to dip below 1 million policies by the end of 2024. These storms could put that goal in jeopardy.

Chuck Nyce: When losses get really bad, that’s when the state should come in. When they get really, really bad, that’s when the federal government should come in. But for the storms like Helene, that should be private market stuff that’s handling those types of things. But it’s an issue we have, yeah.

Simone Del Rosario: Nyce says from an insurance perspective, homeowner policies used to be considered low-risk and relatively stable. But that’s no longer the case in much of the United States. And that’s when we see the private market disintegrate.

Chuck Nyce: If we can solve it in Florida, it’ll be a great lesson to take to other states.

Simone Del Rosario: Because it’s not just hurricanes in Florida and Louisiana. It’s wildfires in California. It’s tornadoes in the Midwest. It’s severe convective storms hitting everywhere in between. Florida may be the tip of the spear for storm exposure, but it doesn’t stand alone.

Straight to your inbox.

By entering your email, you agree to the Terms & Conditions and acknowledge the Privacy Policy.

MOST POPULAR

-

Getty Images

Getty Images

Democrats in Congress receive lowest approval rating in Quinnipiac poll history

-

Getty Images

Getty Images

AG Bondi reviewing Epstein documents for release, could hold client list

-

Getty Images

Getty Images

Speaker Johnson won’t support DOGE stimulus checks

-

Reuters

Reuters

UN chief reveals his plan for peace in Haiti to Caribbean leaders